Swiss equities – Pricing power will become even more important

December 2023

Challenges and opportunities: Click here to read GAM's investment managers' Outlooks for 2024

The Swiss equity market faced another challenging year in 2023, after a difficult 2022. Share prices recovered massively from Oct 2022 to May 2023, but then underwent a major consolidation. The market was largely driven by macroeconomic factors and at the beginning of this year there was optimism that global economic growth would recover. However, the pandemic-induced recovery and the resulting strain on supply chains led to higher inventory levels. Initially, it was expected that the inventory adjustment would be over in the first or second quarter, but it took longer than anticipated. We expect this process to have been completed by the end of 2023.

The impact of interest rates and currency movements on Swiss equities

The Swiss equity market is highly sensitive to the current economic data and the resulting fluctuations in interest rates, especially after the interest rate hike in 2023. Swiss equities have faced downward pressure on their valuations due to the global increase in interest rates; as interest rates rise above negative or near-zero levels, investors have found alternatives to equities.

Another challenge for Swiss companies is the appreciation of the Swiss franc against all major currencies in 2023. This reduces their earnings in Swiss franc terms, as most of their revenues are generated abroad. However, Swiss companies have adapted to the strong currency and have not lost their competitive edge in the recent past. The strong Swiss franc motivates them to enhance their cost efficiency and productivity. Moreover, the inflation rate in Switzerland is significantly lower than in other countries at around 2.2% for 2023, which implies lower wage pressure.

Company performance and prospects

Most Swiss companies coped well with the inflation shock in 2022. They passed on the higher costs to customers, and leveraged their pricing power to maintain or even slightly improve their margins. Switzerland has a large number of companies with high market shares and business models with high barriers to entry, which enable them to enforce higher prices. During the pandemic, companies were generally able to raise their prices, but today it is only possible if a company has a strong competitive position. As the reopening of supply chains is creating price competition, we believe pricing power will become even more important in the current environment.

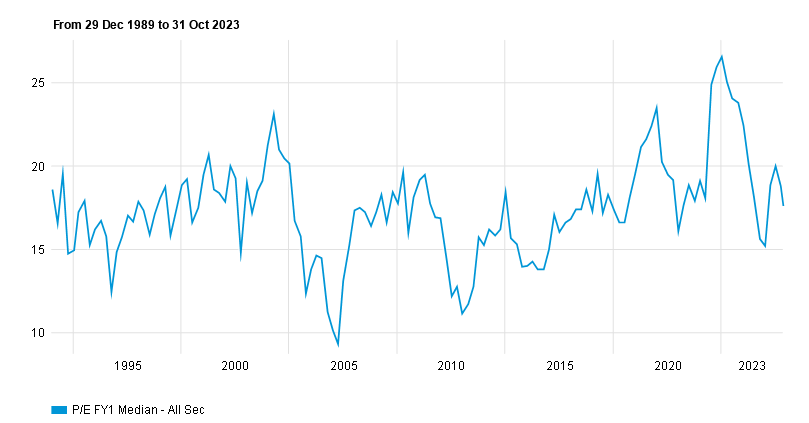

P/E median for Swiss companies near long-term average range

Source: GAM Equity Analytics, Bloomberg

Past performance is not an indicator of future performance and current or future trends.

Our investment strategy

We are strongly focused on companies with high earnings growth and high return on capital, which are able to successfully reinvest capital in the business. We favour profitable, high-quality and well-managed growth companies with healthy balance sheets that can gain market share over time and achieve sustainable value creation. These companies have the ability to invest in research and innovation, develop new markets and expand sales despite crises, and emerge stronger from the downturns. The Global Purchasing Managers’ Index (PMI) has been declining for more than a year. We anticipate a recovery over the course of 2024. This should provide a tailwind for small and mid caps, which we favour. However, if the economic slowdown persists, our companies should be resilient thanks to their healthy balance sheets and margins. We believe market leaders can grow disproportionately faster in the next upturn. Valuations are reasonable – most stocks are trading near their historical average Price to Earnings (P/E) ratios, and therefore the Swiss equity market has become more attractive for medium and long-term investors.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.