Goro Takahashi and Lukas Knüppel, Investment Directors, Japan Equities, explore how various global and domestic factors have contributed to an optimistic outlook for the Japanese equity market.

4 December 2023

The Japanese equity market has been one of the best performers so far in 2023, with the Tokyo Stock Price Index (TOPIX) up 25.9% year-to-date as at 27 November 2023. This outperforms the S&P 500 index, which is up 18.5% over the same period. One of the reasons for the strong market performance is the value rally in Japan. We have seen consistent outperformance of value over growth and quality, and the driver behind this spread is the upward movement of the US interest rate and the Japan Exchange Group (JPX)’s Initiative. JPX requested listed companies to improve their return on equity (ROE) and also the price-to-book ratio (PBR), with a focus on companies with lower ROE and lower PBR and that are in the value category. While value stocks have been outperforming growth stocks, we believe growth and quality stocks are also poised for a bright future, given that US interest rate is peaking out and that growth and quality stocks are better positioned to prove their earnings power and capital efficiency.

Bank of Japan’s policy shifts and wage outlook in Japan

In Japan, the combination of high input costs due to increased prices of imported raw materials and loose monetary policy has led to a depreciating yen. This has triggered inflation in Japan after three decades, which is welcome news for Japan’s policymakers since it allows its economy, mired in decades of stagnant growth and deflation or disinflation, a chance to break out by triggering private investment-led growth.

As Japan is witnessing inflation for the first time in decades, it could be an opportunity for the Bank of Japan (BoJ) to move to a path of interest-rate normalisation. Japan's Finance Ministry might raise the assumed interest rate paid on bonds in the government's annual budget proposal for the first time in 17 years in fiscal year 2024, reflecting policy shifts by the BoJ that have allowed yields to rise. The BoJ policy is expected to hike rates slightly next year, although it will not be as dramatic as we have seen in the US or in Europe. However, there is still a small uptick in yields in Japan; the banks in Japan have also performed quite well in the past two years in anticipation of this. Should the BoJ raise rates next year, this would be quite a contrast to what we are expecting from other central banks, the Fed, and the European Central Bank, where we expect them to reduce rates next year. Hence, we think the yen currency will strengthen next year.

Although there is a growing expectation that the BoJ may end its long-standing negative interest rate policy in 2024, it also depends on the wage outlook going forward, which is uncertain. Despite the continuous inflation over the past two years, the wage hike has lagged behind, resulting in a decrease in real wages. Large listed companies have announced wage hikes, which is a positive sign for the economy. However, it remains to be seen if such hikes will happen in mid to small-cap companies as well. Once we can confirm the recheck nationwide, the BoJ will have more options in terms of controlling negative yield.

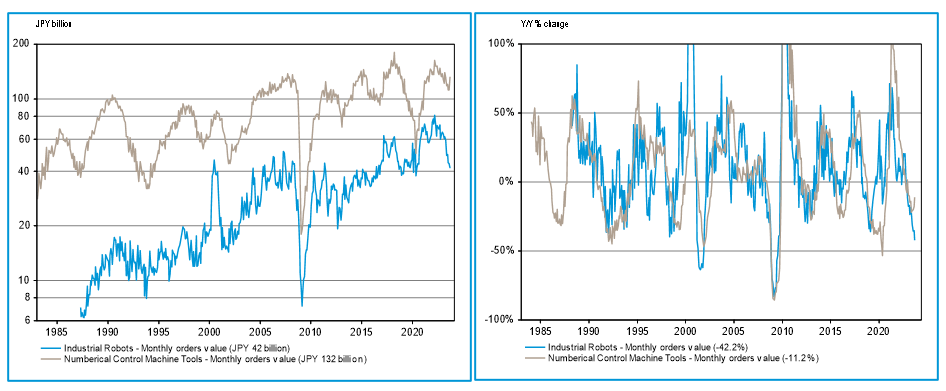

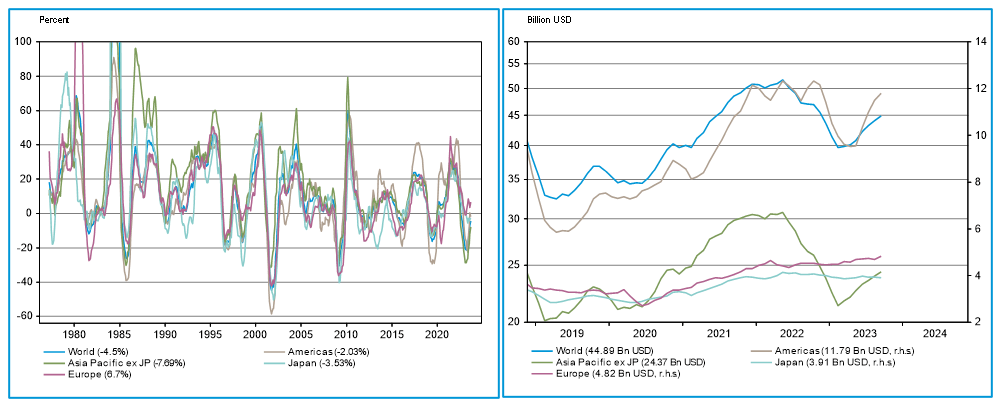

Industrial Robotics and Machine Tool Orders in Japan

One of the key indicators of the industrial sector in Japan is the monthly statistics of industrial robotics and machine tool orders. These reflect the demand and investment in automation and manufacturing, which are essential for the competitiveness and innovation of Japanese firms. The charts below show the year-over-year growth rates of these two statistics, as well as world semiconductor sales, which are important for both the Japanese equity market and the Japanese economy.

Japan – Robotics orders

Source: Refinitiv Datastream, data as at 01 December 2023

Past performance is not an indicator of future performance and current or future trends.

World – Semiconductor sales by region

1 year percent change, 3-month average (left), absolute (right), WSTS data

Source: Refinitiv Datastream, data as at 01 December 2023

Past performance is not an indicator of future performance and current or future trends.

As we can see from the charts, industrial robotics and machine tool orders have been in a down cycle for the past two years, reaching lows comparable to the 2020 Covid crisis. However, we expect they will show a recovery soon, as the fundamentals continue to improve. We have heard from our portfolio companies that they are making progress in the inventory correction, which means that they have reduced the excess stock of their products and are ready to ramp up production and sales. This is also supported by the strong uptake in the world semiconductor sales, which indicates a robust demand for electronic components and devices, especially from the semiconductor production equipment sector, where Japan has a significant exposure.

The service sector in Japan has also been doing very well this year, as the country has recovered from the Covid pandemic and resumed its normal activities. One of the most notable signs of this recovery is the tourism industry, which has bounced back to the pre-Covid levels of foreign visitors. This is a positive development for the Japanese economy, as tourism contributes to the consumption and employment growth, as well as cultural exchange and diversity.

Another factor that affects the performance of Japan equities is commodity prices and logistics costs, which influence their input costs and margins. These have been on a downward trend since the peak in mid-2021, which was driven by the supply chain disruptions and the pent-up demand after the lockdowns.

We expect that this trend will continue in 2024, as supply chain issues are resolved and demand normalises. This would provide a tailwind for companies, as they would benefit from lower input costs and higher profitability. From a fundamental perspective, we are positive for the next two years in terms of earnings growth.

Positive Outlook

The outlook for Japanese equities is favourable, in our view as many stocks are currently attractively priced, on both a relative and an absolute basis, with improving corporate governance and growth. For investors, we feel this presents a compelling opportunity to capitalise on the tailwinds supporting the Japanese equity market.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Past results are not necessarily indicative of future results. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Past results are not necessarily indicative of future results. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.