GAM Investments’ Rob Mumford considers what could be in store for Chinese and Asian markets in 2022, including the impact of a policy shift in China and concerns around US dollar strength.

03 February 2022

2021 was a year of diverse returns for Asia with buoyant Taiwan rising 24%, supported by developed world technology demand, and India rising 25%, due to strong policy support. These were offset by South Korea’s mediocre performance (down 10%) due to a memory downturn and early interest rate hikes. South Asia continued to be negatively affected by Covid-19 (ASEAN -3%), while China moved to aggressive counter-cyclical tightening and aggressive regulatory reform leading to falls of -23% for MSCI China Index, -38% for MSCI China Overseas Index and -6% for domestic A-shares.

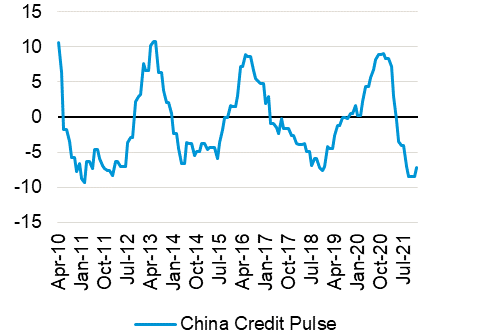

Our expectation for 2021 was for recovery, rotation and reflation, though with modest equity returns as policy withdrawal impacted markets starting first in China while any form of tightening would lag in South Asia. Even with the cautious stance on China early in the year, we did not expect such an aggressive cyclical shift nor such tenacious regulatory reform heading into the leadership transitions in 2022. China completed a peak to trough monetary adjustment over nine months where typically this would occur over 12 to 18 months.

The nationalisation of after school tutoring and forceful de-leveraging of the property sector proved to be beyond most bear case scenarios, with the latter particularly damaging to market sentiment given its large direct and indirect impact on the domestic economy. Coupled with a severe energy shortage, component shortages and Covid-19 disruption, this led to a Q4 growth path significantly below expectations driving an equity de-rating (MSCI China Index -9% over November and December) particularly in cyclically and policy exposed stocks.

China is likely to continue to be the key swing factor of absolute and relative index performance this year. Following last year’s aggressive counter-cyclical policy and social-economic adjustment it now presents an idiosyncratic proposition in the context of a global economy heading towards policy withdrawal and at the very least presents attractive diversification exposure.

Chart 1: China Credit Pulse

Source: Bloomberg as of 31 December 2021. Past performance is not a reliable indicator of future results or current or future trends. For illustrative purposes only.

A key working group headed by the top leadership in December 2021 made a clear signal of a policy shift to an easing stance with sustaining growth the key target. There is a perception in some circles that the priorities of a social political agenda, including dual circulation and common prosperity, may preclude any urgency to deal with the current negative economic trends in growth. We do not concur with this view and with both systemic risks (including unforeseen outcomes of property de-leveraging) and unemployment risks from last year’s cyclical and regulatory adjustments, a more pro-growth agenda will emerge this year into the leadership transition sessions which will occur later in 2022.

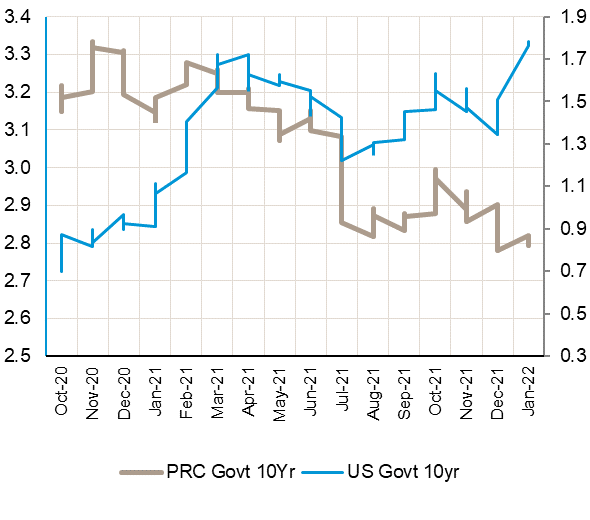

Chart 2: China 10-year government bond versus US 10-year government bond

Source: Bloomberg as 31 December 2021. Past performance is not a reliable indicator of future results or current or future trends. For illustrative purposes only.

Our favoured positioning in China equities is to policy sensitive, deep value and we remain in attractive policy aligned sectors. China equities are likely to get a further boost if the pace of social-economic adjustments ease (particularly property) and more focus is given to halt the negative economic growth trends. A shift to a structural positive view depends on trends in the depth and breadth of the more recent accelerated focus on dual circulation, common prosperity and the role of the state effecting quasi and outright private enterprise.

Regionwide (ex-China) with vaccine coverage and herd immunity reaching positive levels, both a consumption and private investment recovery is expected. By the end of Q1, 11 out of 12 Asian countries are expected to have first dose vaccination rates over 80%, according to estimates by Morgan Stanley. In addition, given slowing but still elevated global growth, trade activity is expected to remain buoyant, combining to present an attractive consumption, investment and capex environment supportive to earnings.

From a policy standpoint, inflation expectations are fairly subdued on current forecasts which means the region could experience a much lower negative fiscal and monetary pulse versus developed world while China is highly likely to receive both a monetary and fiscal positive boost weighted into H1 2022.

The key groupings for the rest of the region include North Asia which will be the most sensitive to developed world growth path and policy shifts and South Asian economies with a domestic focus and recovering from another year impacted by Covid-19.

We see North Asia starting the year supported by strong developed world economic momentum and the derivative impact of strong trade trends and regional recovery (hopefully with China becoming a tailwind this year) driving strong capex momentum.

South Asia and India offer attractive cyclical and structural profiles without the endemic problems of more advanced economies (including North Asia/China) faced with challenges across demographics, inequality, indebtedness and deflationary forces.

From a structural perspective positive demographics and low indebtedness can drive growth at elevated levels supported by government initiatives including new infrastructure and renewable investment. 2022 is likely to see a strong recovery in private investment supported by production shifts out of China and ongoing elevated trade activity driving a strong capital expenditure and consumption outlook.

The key risks include disorderly US inflation driving policy rates higher than current expectations and a stronger US currency either from a rate differential or risk off perspective. The recent pull back in the USD reflects real rates that will still stay low for some time even on more recent more hawkish forecasts while other more cyclical regions and currencies could perform relatively better. Concern regarding USD strength, recent underperformance, China and potential US interest rate curve flattening (which could drive higher equity risk premiums) are reasons for the current consensus underweight positioning across emerging equities.

However, the current scenario of ongoing earnings growth offsetting rising interest rates and China shifting to an easy stance, coupled with attractive valuations, could drive a positive positioning tailwind. Even a small positioning switch back to emerging markets (EM) can drive large positive relative moves given the relative lower liquidity of EM equities versus developed market equities and potentially cross over from credit markets.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.