China’s long-awaited reopening following the Covid pandemic, presently underway, is both similar to and different from earlier ones in the US and Europe, as well as China’s own initial reopening in 2020. Jian Shi Cortesi and Swetha Ramachandran outline the drivers and likely beneficiaries of an expected sharp resurgence in Chinese consumption in 2023.

01 February 2023

The advent of Chinese New Year – the first in China since 2019 without any Covid restrictions, brings with it the end of the year of the Tiger and the beginning of the year of the Rabbit. At the same time, the easing of China’s zero-Covid policy has granted the Chinese economy and markets a much-anticipated boost for the rest of 2023. We are reminded of another rabbit – the White Rabbit from children’s classic Alice’s Adventures in Wonderland, fretting anxiously: “Oh dear! Oh dear! I shall be late!” Investors who have seen the Chinese market as well as China-exposed stocks rebound materially since November may share this sentiment of having ‘missed out’ on the Chinese recovery story. However, we believe that the coming upturn in Chinese consumption is far from priced into share prices of Chinese equities or global equities with a significant China consumer exposure (including luxury stocks) as we expect the pace and extent of demand recovery both to exceed current market expectations.

Where are we now? Covid, of the Omicron variant, has been spreading rampantly in China since the country took its first steps towards a full reopening in December. It appears to have exhausted itself in urban China, which is home to two-thirds of Chinese, before the Chinese New Year festivities likely spark a further wave in rural areas, the end of which is expected to mark the ‘return to normal life’ after three years. Traffic is already noted to be rebounding strongly in large cities with intra-city mobility returning close to pre-pandemic levels and demand for travel during the New Year holidays up significantly within China.

Where are we headed? While the relaxation of Covid restrictions in China may not be all smooth sailing, China’s reopening is already being noted to have a substantially positive impact on the domestic economy as ‘pent up’ demand starts to be unleashed into the Spring Festival. Even people electing not to travel over the holiday period are likely to spend more money on local goods and services this year compared to previous years, with retail, catering and entertainment businesses allowed to operate without any restrictions. In the US and Europe for example, the reopening was marked by a gradual reversal of spending away from goods into services (such as recreation, dining out of the home) – with the latter not being an option for consumers during lockdowns. As in the West, we are likely to see the pendulum shift sharply back towards bricks and mortar retail from online in the immediate term, as consumers rediscover the joy of instore shopping and offline entertainment and experiences. Recent surveys suggest the top three activities Chinese consumers want to participate in post Covid are: travelling, dining out and exercise outdoors.

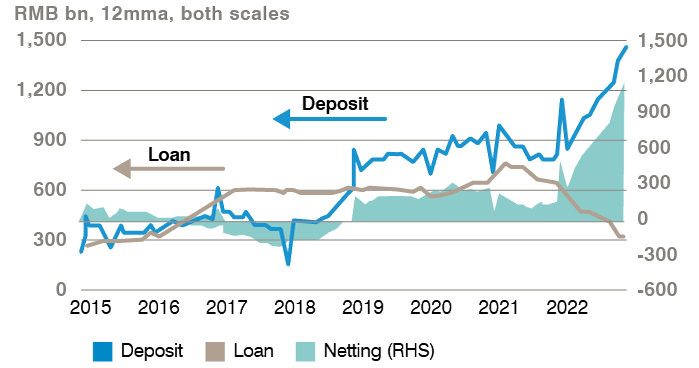

Recovery, with Chinese characteristics. One key difference between Chinese and US households is that Chinese households have had high savings rates historically – in the 30%+ range compared to 5-6% in the US, even before the pandemic, before rising to a record 38% in 2020. Chinese consumers are now going into reopening with strong household balance sheets. The below-trend consumption activities in the past three years (due to reduced movements and cautious consumer sentiment) have led to a large amount of excess savings. Estimates attempting to quantify the amount of excess savings vary widely by source – ranging between RMB 4-10 trillion – or 6-12% of GDP sitting in excess savings.

It is useful to recall that it was China where the phenomenon of ‘revenge spending’ first occurred in 2020 – after China was ‘first in, first out’ from the initial innings of the pandemic – leading to consumers spending freely in a wave of post-lockdown euphoria. The difference this time is that consumers have had (nearly) three years’ worth of accumulated excess savings versus three months in 2020 with an even greater amount of pent-up demand having built up.

Chart 1: New increased household deposit and loan

Source: PBOC, JP Morgan. For illustrative purposes only.

Chart 2: Cumulative excess saving since 2020

Source: NBS, JP Morgan. For illustrative purposes only.

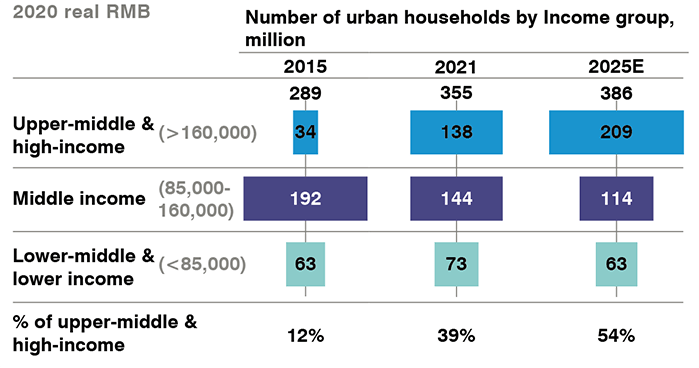

We also see the policy backdrop as being supportive for consumption. According to China State Council’s Strategic Guidelines on Expanding Domestic Demand 2022-2035, the government will continue to promote traditional consumption such as housing and cars, while vigorously developing services consumption including tourism, sports, childcare, and elderly care. Recent comments around ‘common prosperity’ continue to emphasise the expansionary nature of the policy for all, rather than a redistribution of income, with the ultimate aim to double the size of China’s middle class to 800 million by the end of the current decade.

Who stands to gain from China’s reopening? We have identified the likely ascent of offline to online as well as the pent-up demand for dining out of the home and physical retail as likely beneficiaries. We expect Chinese companies exposed to discretionary spending – which will be supported by household savings – to benefit particularly, such as hotels, airlines, movies, restaurants, sportswear, and cosmetics. We expect global luxury brands to gain significantly from the ongoing resumption in international Chinese tourism, the return of the ‘feel good factor’ among consumers, as well as the skew of household savings disproportionately towards higher income groups who are these brands’ target consumers. We note that beneath the current wave of reopening, the structural trends driving China’s consumer potential – namely, the expansion of the middle class, as well as ‘consumer upgrade’ (trading up) remain intact and supportive.

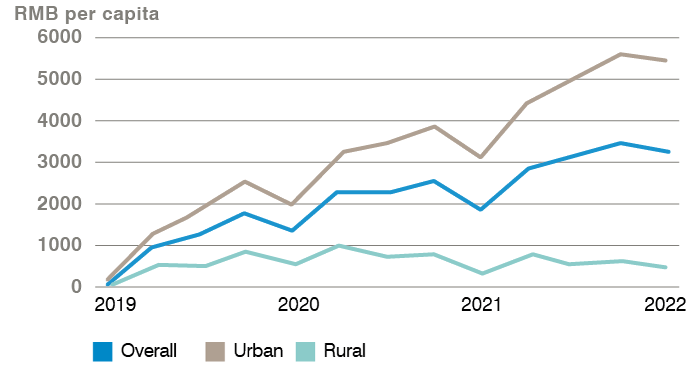

Chart 3: Annual household disposable income in China

Source: McKinsey 2023 China consumer report. For illustrative purposes only.

China remains a dynamic and exciting consumer story for global investors and as active investors, we remain alert to ongoing developments in this market and the implications for our investments. After all, as Alice of Alice's Adventures in Wonderland herself says, “I could tell you my adventures—beginning from this morning, but it’s no use going back to yesterday, because I was a different person then.”

Important disclosures and information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. There is no guarantee that forecasts will be realised.

This document contains forward-looking statements relating to the objectives, opportunities, and the future performance of the markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.