A year ago, the Credit Suisse crisis reverberated through European bank bonds. As we mark the anniversary, Atlanticomnium’s Romain Miginiac delves into the dynamics and future prospects of the AT1 market.

20 March 2024

The one-year anniversary of the infamous Credit Suisse (CS) Additional Tier 1 bond (AT1) write-down is a good opportunity to reflect on the AT1 market. Unsurprisingly, CS’s write-down of AT1s has not triggered the death of the asset class, as highly attractive yields against a backdrop of rock-solid fundamentals have trumped the initial negative sentiment of close to 8% of the market being wiped out.

Nearly 12 months post CS, the impact has now been fully digested. The recovery has been truly spectacular – three points below illustrate the normalisation of the market:

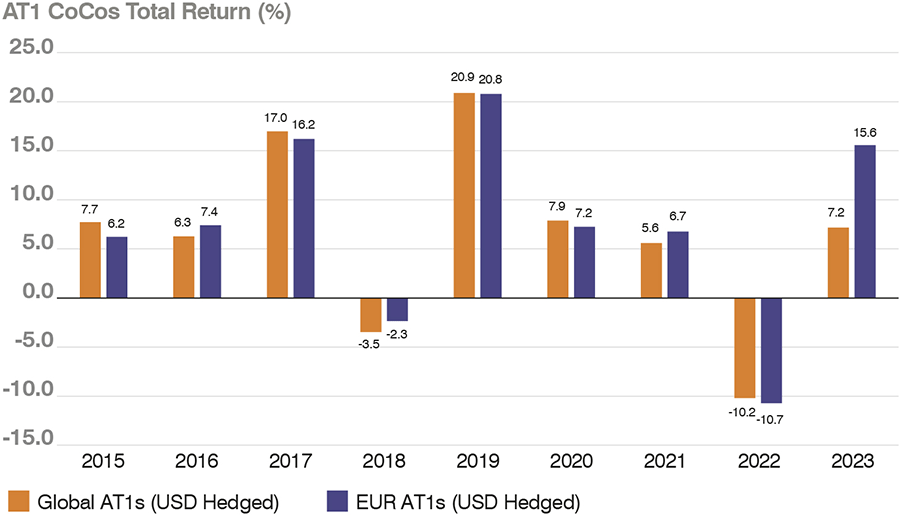

- Strong total returns in 2023: 2023 ended up being a strong year for AT1 investors; total returns on global AT1s (hedged in USD) were above average at +7.2%, including more than 5% impact from CS. Looking at the EUR-denominated AT1 contingent convertible bond (CoCo) universe that did not include any CS bonds, these delivered a very decent return of +15.6% in 2023, the third best year on record.1

- AT1s are now cheaper for banks to issue than pre-CS: Spreads on AT1s are now at 390 basis points (bps), compared with around 400 bps at the tightest level seen pre-CS in early 2023, and below their long-term average of circa 450 bps.2

- The largest orderbook on a new AT1 deal post-CS was from a Swiss bank: UBS’s dual-tranche USD AT1 of USD 3.5 billion issued in November 2023 attracted more than USD 36 billion of demand, more than 10 times oversubscribed. This record demand is equivalent to more than 15% of the whole AT1 market (in terms of market value), reflecting very strong demand for the asset class. New deals have typically been oversubscribed multiple times, as demand has not faltered compared to history.3

Chart 1: AT1 performance has been strong in a challenging year

Source: Atlanticomnium, Bloomberg, as at 10 March 2024.

Where do we go from here?

AT1s had a strong run in late 2023 and early 2024, delivering double digit returns since the start of Q4. We continue to see AT1s as attractive, offering high carry with further price upside potential.

With yields of circa 8% on AT1 CoCos and spreads of just below 400 bps – the AT1 CoCo market remains one of the highest yielding asset classes within liquid credit. Bondholders can potentially benefit from the robust credit quality of European banks, generating structurally higher profitability and sitting on large excess capital buffers.

Spreads have tightened, yet remain wide compared with the lows that we have seen in past cycles, circa 270 bps in early 2018 for example. We believe bondholders will continue to benefit from a larger earnings buffer and continued strengthening of the European banking sector. To illustrate, no EU banking system has a non-performing loan (NPL) ratio above 5%4, and no bank in the STOXX Europe 600 Index is expected to make less than 6% return on equity during 2024 to 20255. As fundamentals and valuations converge, we believe there is upside for bondholders as spreads tighten.

This is at a time when spreads on investment grade (IG) and high yield (HY) bond markets have returned to close to their lowest levels. Comparing AT1s to the US high yield market for example, spreads in HY bonds are at a much tighter level (circa 300 bps) and materially closer to the lowest levels over the past decade, so we believe AT1s offer close to 100 bps pickup in spread, not far off the highest levels seen over the past decade.

Extension risk remains overpriced in our view, as around a third of AT1s are not priced to their next call date. In 2023, 93% of AT1s were called at their first call date, in line with the 94% long-term track record of European banks. Looking ahead to 2024, more than 60% of AT1s have either been called or already pre-financed, and we expect that at least 90% of AT1s will be called. As bonds re-price to call, this should lead to material upside, in our view.

Subordinated debt remains a sweet spot

AT1 CoCos and subordinated debt of financials more broadly, remain at a sweet spot in credit markets, in our view. We feel the asset class allows investors to capture attractive yields from a strong sector, with further upside potential as spreads tighten and bonds re-price to call. In a soft-landing scenario with inflation under control, where central banks are expected to cut rates, the asset class offering some of the highest yields in the market is likely to benefit strongly from a renewed hunt for yield.

1 Source: Atlanticomnium, Bloomberg.

2Source: Atlanticomnium, Bloomberg.

3Source: Atlanticomnium, Bloomberg, company documents.

4Source: European Banking Authority.

5Source: Atlanticomnium, Bloomberg.

2Source: Atlanticomnium, Bloomberg.

3Source: Atlanticomnium, Bloomberg, company documents.

4Source: European Banking Authority.

5Source: Atlanticomnium, Bloomberg.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

Certain information provided herein is based on third-party sources, which information, although believed to be accurate, has not been independently verified. GAM assumes no liability for errors and omissions in the information contained herein. This article is for informational purposes only and may not be reproduced or distributed without the prior consent of GAM.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

Certain information provided herein is based on third-party sources, which information, although believed to be accurate, has not been independently verified. GAM assumes no liability for errors and omissions in the information contained herein. This article is for informational purposes only and may not be reproduced or distributed without the prior consent of GAM.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.