European banking stocks have delivered impressive returns so far in 2024 (+16.7%* for the sector). Niall Gallagher assesses the factors behind the gains, and explains why he is retaining heavy overweight exposure to European banks.

25 April 2024

We have held significant overweight exposure to European banks for three years and maintain our view that the sector is very attractively valued.

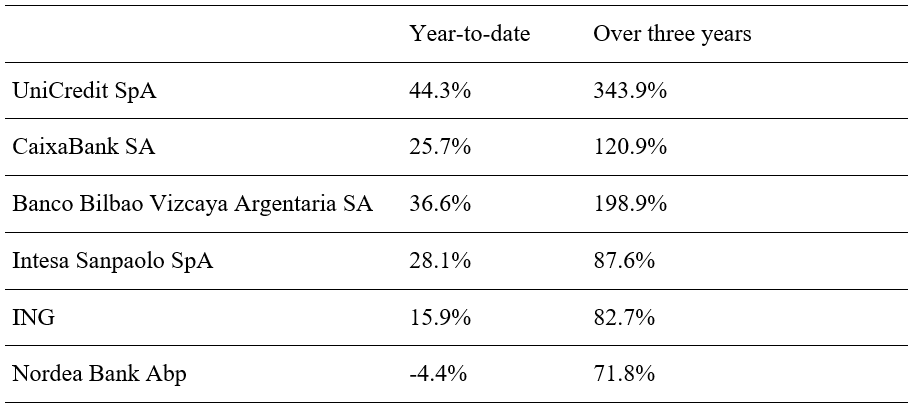

Figure 1 shows the total return for the five traditional banking stocks we favour, showing that all of the stocks - apart from Nordea - have significantly outperformed the European market (which is up +7.3%1 year-to-date). Judged over the three years since our initial interest in banks – since when the European market has risen by 29.1%2 - the performance is even more impressive (full disclosure: we have not owned all of these stocks for entire three years). So the sector has done very well.

Figure 1: European bank stock: total returns

Source: Bloomberg. Year-to-date based on 29/12/23 to 4/4/24, three years based on 1/4/21 to 4/4/24. The mentioned stocks are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice.

*MSCI Europe Banks Net Return EUR Index, 29/12/23 to 4/4/24, source: MSCI.com

1Source: GAM, MSCI Europe Index in EUR Net Total Return 31/12/23 to 4/4/24

2Source: GAM, MSCI Europe Index in EUR Net Total Return 4/4/21 to 4/4/24

1Source: GAM, MSCI Europe Index in EUR Net Total Return 31/12/23 to 4/4/24

2Source: GAM, MSCI Europe Index in EUR Net Total Return 4/4/21 to 4/4/24

For those of a ‘technical analysis’ disposition, the Relative Strength Index (RSI) of each of these stocks (apart from Nordea) is over 80 – a level typically considered to be in ‘overbought’ territory, so it is a reasonable question to ask whether the outperformance in European banks is ‘done’ or whether the valuations are stretched in the short-term.

Whether European bank stocks are overvalued or not in the short-term, we must remember that an RSI is a short-term trading indicator only and tells us nothing about the fundamentals, or valuation of the stocks, and importantly, the starting point of the outperformance. It is these factors we need to look at when considering whether the performance cycle of our banking stocks is coming to an end from an ‘investment perspective’; an ‘overbought’ RSI can normalise through the stocks selling off, or through the stocks pausing for a short period. To predict which is more likely to occur we need to reconsider the investment case.

Despite the gains, valuations remain cheap

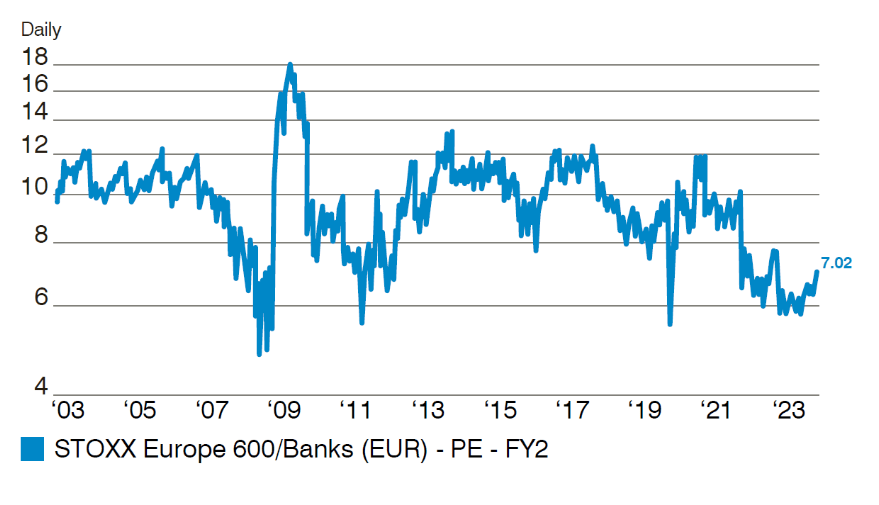

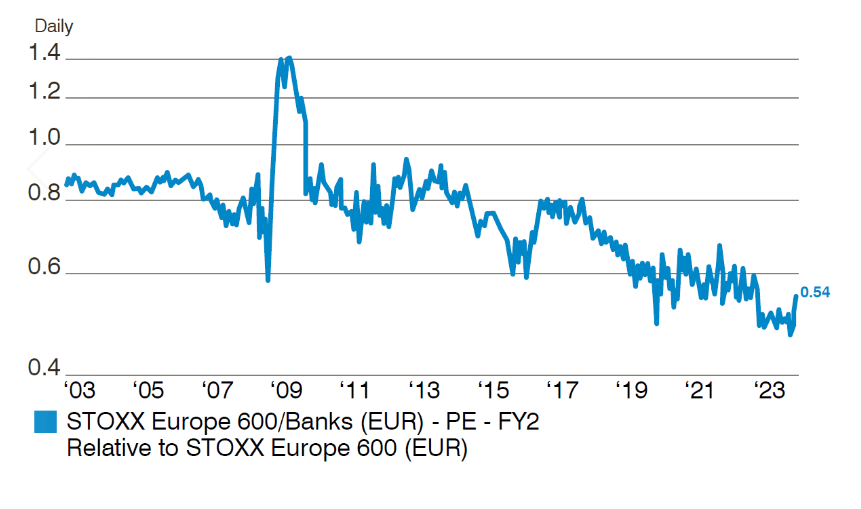

First of all, let us look at valuation, remembering that for most of last year the European banking sector was trading at some of the lowest valuations in stock market history: Figure 2 shows that the PE multiple has risen from under 6x to just over 7x. But this compares to a long-term average of over 9x, while on a Price Earnings Relative basis (to the broader market) the PER has gone from 0.48x to 0.54x versus a long-term ‘normal’ of 0.8x. These two metrics suggest that there is somewhere between 35-50% upside to get to either an average valuation multiple, or to establish a normal relationship with the rest of the market – on that basis, the sector remains cheap in valuation terms.

Figure 2: European bank sector PE multiple

Figure 3: European bank sector Price Earnings Relative

Source: Factset

What about the case for earnings/profits to fall, as many are calling for, as the interest rate cycle rolls over?

We have been clear in all of our communications that the rise in central bank interest rates from -0.5% to over 2% has been transformational to the profitability of European banks, leading to a more than doubling of sector Return on Equity. But we also think that many fundamentally misunderstand the relationship between banking sector profitability and interest rates. In most interest rate environments there is little relationship between the level of central bank interest rates, or bond yields and European banking sector net interest margins, revenues and earnings / Return on Equity but the overall relationship between rates/yields and bank earnings is non-linear / asymmetric where at most levels there is no relationship at all, but at very low levels of central bank interest and yields (sub 1.5%) the impact on bank earnings is very negative indeed. That is to say, ultra-low or zero interest rates/yields are very negative for bank earnings / Return on Equity but otherwise interest rates and yields really do not matter much at all, with competitive intensity far more significant.

Zero chance of a return to ZIRP? (Zero Interest Rate Policy)

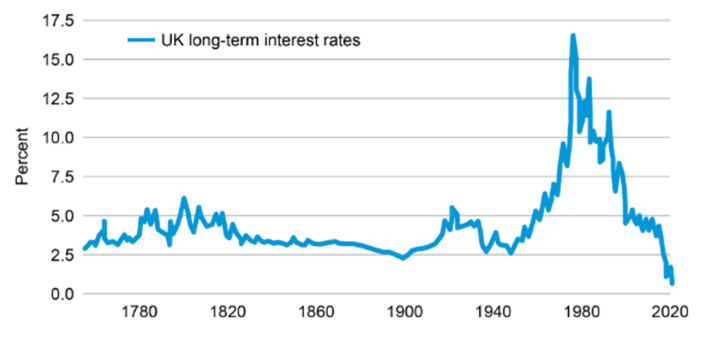

For the many reasons we have outlined at length over the past three years as to why we do not think we are going back to zero rates again (in our lifetime) as the global economy has a number of inflationary influences driving it, but for those who are sceptical of this it is worth looking at figure 4 which shows 300 years of UK interest yields, illustrating just how extraordinarily unusual the period 2008-2021 was. There is no period comparable period to 2008-21 in modern history and many economists are beginning to question whether zero rates and quantitative easing (QE) were major policy errors that have created great economic distortions.

Figure 4: UK interest rates over the last 300 years

Source: GAM

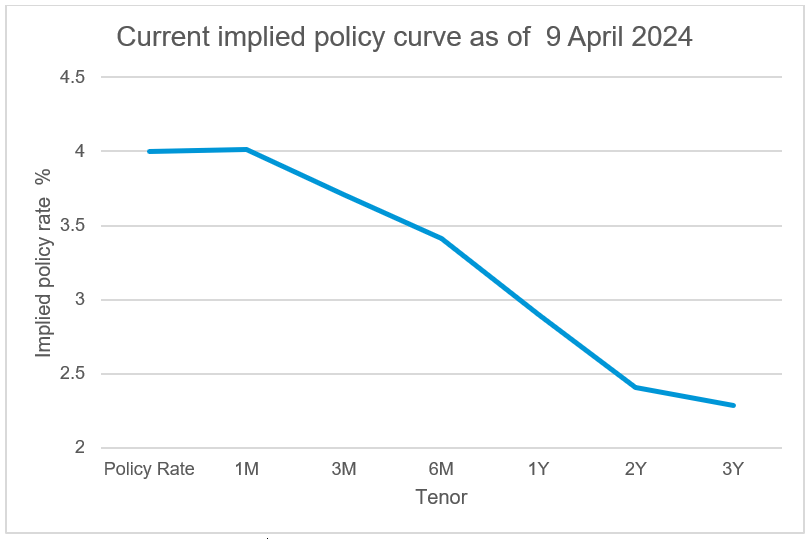

For interest, figure 5 shows the market implied interest rate path (from bond yields) for the Eurozone, illustrating that the market does not believe rates will go below 2.25% within the next three years, a fairly good estimate of the terminal ‘dot’.

Figure 5: Eurozone market-implied interest rate path

Source: Bloomberg, GAM

Is there anything else that could cause sector profitability to crack?

We think it unlikely that there will be much of a credit cycle (ie, loan losses) as the sector has spent much of the last 15 years deleveraging - there really is not a lot of risk on bank balance sheets and this deleveraging is also reflected in consumer and business sectors in many European economies. Furthermore, the sector has been through a serious amount of consolidation, thereby reducing competitive intensity, so there is not much risk of price wars bringing down profitability either. And with far higher levels of equity capitalisation the sector has also seriously embraced share buybacks such that, even with the strong performance year-to-date, most of the stocks have a total distribution yield of greater than 10%, and this is likely sustainable for the next few years.

So, to summarise, while the sector has done very well year-to-date and there is a short-term risk of ‘consolidation’ or minor underperformance into any Q1 disappointments, in our view, the fundamentals remain compelling, and the sector cheap. Therefore, we are going to remain very overweight.

Important disclosures and information

Past performance is not an indicator of future performance and current or future trends. The performance is net of commissions, fees and other charges. Allocations and holdings are subject to change. The views are those of the manager and are subject to change. There is no guarantee that forecasts will be realised.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

Past performance is not an indicator of future performance and current or future trends. The performance is net of commissions, fees and other charges. Allocations and holdings are subject to change. The views are those of the manager and are subject to change. There is no guarantee that forecasts will be realised.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.