GAM Investments’ Niall Gallagher considers why the market remains too pessimistic on European banks and outlines five reasons why he believes the sector represents an opportunity.

18 May 2023

2023-to-date has been characterised by significant turbulence in the US regional banking sector. In March, we saw the collapse of Silicon Valley Bank, and in April the failure of First Republic Bank and the sale of its remains to JPMorgan Chase. Read across from these events has led to the poor performance of the European banking sector year-to-date, but we believe European banks are in a very different position to US regional banks – with the takeover of Credit Suisse by UBS in Switzerland in March an idiosyncratic case. Indeed, we have stated for some time that the market remains too pessimistic on European banks and as the Q1 results season draws to a close a number of points on the strength of European banks are clear:

- European bank Q1 earnings have come in well ahead of expectations, leading to continued upgrades in estimates for 2023 and 2024 earnings. The beats and upgrades have come from much higher net interest income, a result of the impact of rising interest rates on bank balance sheets and profits. The move from negative to positive interest rates in Europe – and a normalisation of rates to more historic levels – was at the heart of our thesis that European bank profitability would be ‘transformed’, driving a significant increase in earnings and rising return on tangible equity (ROTE). This is what we are now seeing.

-

Deposit books are stable, with very limited deposit outflows (typically 0-2%). During the pandemic, we saw a sharp rise in savings balances, leading the banking sector to hold excess deposits. We would expect banks’ deposit books to slowly decline, which is what we are seeing – but slowly. Loan-to- deposit ratios remain typically at around 80-90% and the liquidity coverage ratios are typically well over 150%, far beyond regulatory minimums.

Furthermore, there is a limited amount of ‘terming out’ of deposits so deposit ‘betas’ remain very low. Essentially, this means banks are retaining most of the benefit of rising interest rates; we would expect this to change over time, but it is changing more slowly than expected and this is positive for earnings.

- There are no signs of credit stress or recession. Loan loss provisions (LLPs) remain below average levels but we think they are still too high given what banks are experiencing in terms of asset quality. We expect to see LLPs come down further this year, driving further earnings upgrades as banks are over provided. The market’s focus has been on commercial real estate (CRE) and although we believe there are reasons to worry about this as an asset class, bank exposures to this sector are low (well below prior cycles) and loan-to-value ratios very low (typically 40-50%). In short, 15 years of deleveraging and balance sheet repair since the Global Financial Crisis has left European bank balance sheets in a very conservative condition.

- Positive momentum on capital returns. The overall distribution yield (dividend yield plus buybacks) for the sector is approximately 12%, with some banks guiding to return close to 50% of their market capitalisations in dividends and buybacks over the next three years and numerous banks trading on dividend yields of close to 10%. Dividend and buyback guidance has largely been raised as we have gone through Q1 reporting season, with the momentum on capital returns remaining positive.

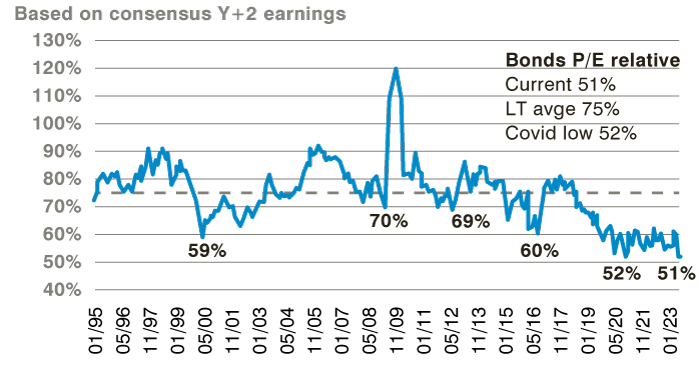

- Valuations for the sector are almost at an all-time low. The sector currently trades on approximately six times earnings, with very strong earnings momentum representing a price earnings relative of around 50% (see Figure 1). This is just about the lowest ever recorded and compares to a long-term average of 80%. On a price-to-tangible book basis, the sector trades on 0.7x for a 12.5% return on tangible equity, while fair value for the sector is 100% above current stock prices and 60% higher on a relative basis.

Figure 1: European banks’ price earnings relative

Source: Autonomous Research

In summary, despite a very positive backdrop, with positive earnings momentum and low valuations, the sector has performed poorly year-to-date as a result of events in the US regional banking sector. Despite this we see no read-across from the US and remain positive about the sector’s prospects. As ever, active, bottom-up stock selection remains key.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This presentation contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.