Does the rising wave of layoffs in the Technology Industry have a silver lining?

03 May 2023

After a decade of strong growth for technology companies which saw them allot significant resources to new projects and people, they are beginning to scale back. Kevin Kruczynski examines how this new focus on profitability may benefit the sector.

Click here to view the Disruptive Strategist newsletter in full.

Over the last decade technology companies have been in all-out growth mode, driven by a combination of strong underlying demand as their products and services disrupted and penetrated existing and new markets, low interest rates which led to an abundance of capital, and an investor base that encouraged management teams to prioritise sales growth over profitability. In this environment it is no surprise that capital misallocation was prevalent and companies with extremely profitable core operations started allotting increasingly more resources to projects that they hoped would open up new growth pathways. Alphabet’s renowned “moonshots” encompassed self-driving cars, delivery drones, smart thermostats, Google Glass and smart contact lenses, which were all supported by cashflows from its extremely profitable Google advertising business. Amazon also decided to pour the profits from its AWS cloud division into various areas ranging from logistics to brick-and-mortar stores and healthcare services. Meta followed suit; having been successful with Facebook, Messenger, WhatsApp and Instagram, it has poured tens of billions of dollars into developing its metaverse. There has also been a trend for hiring ahead of demand. One recruiter hired by Meta claimed she was paid USD 190,000 a year to do nothing. Another former Meta worker hired in April 2022 said “They were just kind of, like, hoarding us like Pokémon cards.”

Many companies in this space pride themselves on being relatively asset light and high margin businesses, so it has been intriguing to see the considerable growth in headcount over the last decade. The increase in employees has almost been seen as a gauge of success, and companies offered increasingly lavish perks to attract talent. Employees were given transportation to the office, where complimentary meals were provided, along with free flowing barista-prepared coffee. Additional amenities typically included on-site wellness centres, massages, laundry services, fitness facilities, live music events, and more… a significant evolution from ping-pong tables and gaming consoles. What initially began as a well-meaning strategy to foster a culture of innovation and creative thinking ultimately transformed into a sense of entitlement and inflated cost structures. Back in 2012, Amazon’s workforce was less than 100,000 strong, but by the end of 2022 it has surged past 1.5 million. A significant portion of these employees work in fulfilment centres and logistics roles. For comparison, FedEx, UPS and the US Postal Service together employ just under 1.4 million individuals. Meanwhile, Meta’s headcount had risen from under 5,000 to over 85,000 during the same timeframe, as the company broadened its scope. Salesforce serves as another example of a company that experienced a tenfold increase in staff numbers over the past decade, choosing to prioritise sales expansion over profit margins.

The Covid pandemic exacerbated the circumstances, as individuals under lockdown were required to work remotely, altering their spending patterns, and resulting in exceptionally high demand for technology. Many businesses mistakenly viewed this as a lasting change in growth trends, and consequently expanded their investments in digital infrastructure, data centres and workforce expansion. During this period, valuations also rose due to lower interest rates pushing discount rates and equity risk premiums down, providing further encouragement for management teams to invest. As economies reopened demand patterns started to normalise, but inflationary pressures fed through to the economy, prompting central bankers to suggest significant interest rate rises were necessary. The inflationary situation was further exacerbated by the conflict in Ukraine, which caused a shortage of many commodities. Consequently, the past year has witnessed the swiftest series of interest rate hikes in decades, dramatically altering the atmosphere in capital markets. As growth rates normalised and valuations decreased, investors are now signalling a preference for companies which focus on growing profits rather than sales.

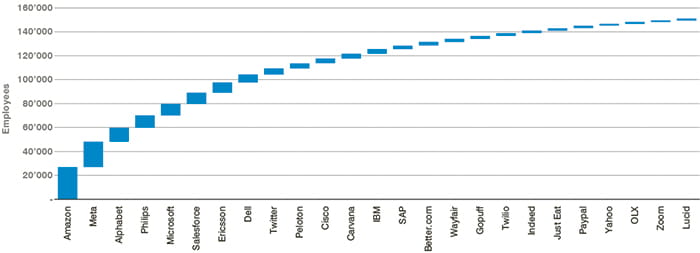

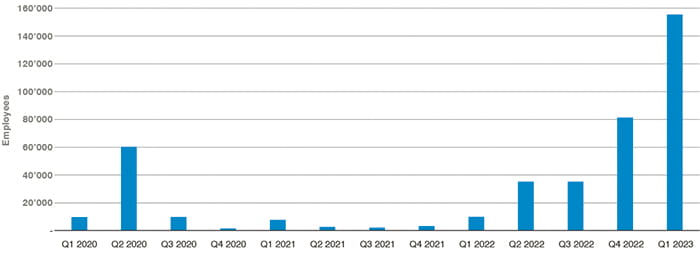

Companies have adjusted their strategies accordingly and are now noticeably more cost-aware with a focus on the most profitable part of their operations, while peripheral projects have been scaled back or closed. As per Layoffs.fyi, more than 310,000 technology positions have been eliminated since the first quarter of 2022, as illustrated in the charts below. It is not a coincidence that the timing of this newfound discipline aligns with the shift in central bank interest rate policy.

Chart 1: Cumulative job cuts in the tech sector from Q1 2022 to Q1 2023

Chart 2: Tech job cuts by quarter

Sources: GAM, Layoffs.fyi, checked against underlying company announcements. As at 31 March 2023.

The share price reaction to this shift in priorities has been broadly positive, as companies are now on a firmer and more economically sound footing. Looking forward, as we transition into the era of artificial intelligence and automation, the potential to further enhance efficiency and productivity is immense. We are carefully examining those businesses which we believe can adopt innovative working methods to increase productivity and profit margins while sustaining their growth path, and the companies that provide the tools to enable them to achieve this.

Important disclosures and information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers.