Gaining traction in the mid-1970s, stock-based compensation was once seen as the golden egg waiting to vest. GAM Investments’ Pieran Maru discusses why there is greater caution around stock-based compensation today and examines some of the challenges associated with it.

30 August 2022

Click here to view the Disruptive Strategist newsletter in full.

Stock-based compensation (SBC) allows companies to reinvest as much cash as possible to further growth, while attracting and retaining talent by compensating employees in the upside of the future stock price. According to the National Center for Employment Ownership, fewer than 1 million people were receiving stock options in 1990; jumping to approximately 10 million in 2000. Although negatively impacted by the dot-com bubble and changes to the accounting rules in 2006 which required companies to recognise SBC as an expense, it continued to gain traction, with nearly all listed companies utilising SBC today.

So why are we more cautious of SBC now? While SBC is used to align employees with the employer, a downturn in the stock price, and therefore the value of SBC, can have a reversal impact, further compounded by the current increase in the cost of living. With a tight hiring market for specialist roles in the software industry, employee churn is likely to increase and in turn, pressure for employers to increase the proportion of cash payments for new hires and retention. Higher cash payments would impact margins, earnings per share (EPS) and free cash flow (FCF) negatively, while offering additional SBC to incentivise employees would in turn further dilute the value for shareholders.

SBC comes in a variety of forms. The two most common types are stock options and restricted stock units (RSUs). Stock options grant the employee the right to buy shares at a set price determined on the day the options are given. The employee then has a set period of time to exercise the options, often one year after the grant date. While for RSUs, the employee is granted stock which vests over time. RSUs are often considered the better option for the employee, as there is no cash paid in issuing them.

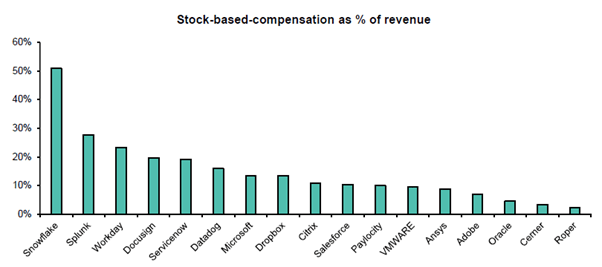

Figure 1 highlights the prevalence of SBC not only in high growth software names such as Snowflake, whereby SBC consists of an outsized ~50% of revenue, but also in more value style names such as Cisco where SBC is hitting double digits. This shows just how impactful SBC can be in the wider software market.

Figure 1: SBC as % of revenue varies massively with the value names using much less SBC (Source: Bernstein)

Overall, we continue to see SBC as an integral part of high growth software companies. However, we expect firms to tighten control of SBC. In preparation for a potential economic downtown, a number of large cap technology companies have already announced a slowdown or pause on hiring which in turn should assist in reducing the rate of SBC growth.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.