The sell-off in 2022 has been both profound and near-universal. GAM Investments’ Julian Howard considers whether there is now intrinsic value in key markets.

14 November 2022

Leo Tolstoy once wrote that “The two most powerful warriors are patience and time.” For investors in 2022, watching the ‘Everything Sell-Off’ without capitulating and selling all their holdings has been a test of both. But the extent and the universality of this year’s drawdowns have pushed many to the limit. A cursory survey of the investment universe reveals the S&P 500 is down -17.7%, the Nasdaq Composite of US Technology stocks is down -29.3%, the 10-year US Treasury note is down -18.4% and US high yield bonds as measured by Barclays is down -12.2% in the year to 31 October. Bearing in mind the old adages about value traps and catching falling knives, the real question for those investors who have grimly held on this far is whether there is now value in these assets which might justify not only maintaining their positions but actively adding to them. And, by extension, if there is value to be had in markets, when might it be realised?

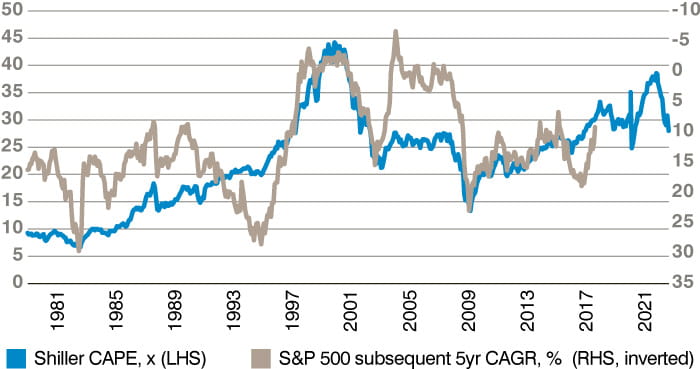

Starting with equities, the S&P 500’s valuation is perhaps best assessed by the Shiller cyclically-adjusted price/earnings ratio, or CAPE. This measure is smarter than the standard price-to-earnings ratio because it takes into accounts earnings over the previous decade and is therefore a fairer assessment of the market’s price over its longer term track record of generating revenue. The Shiller CAPE also provides a good prognostic indicator of future returns, though of course it is no crystal ball. As of the latest datapoint of 4 October, the Shiller CAPE stands at 28x, which is certainly cheaper than its recent peak of 39x in November 2021, and not too much more expensive than the average valuation since the end of 1979 of 23x. Importantly, the current valuation suggests that the S&P 500 might go on to make a compound annual return of around 10% over the next five years. This is virtually the same as the 10.3% return posted by the index in the five years up to 4 October 2022.

Figure 1: Still attractive – Shiller CAPE hints at potential future five-year compound return of 10% per annum

Source: GAM, as at 4 October 2022. Past performance is not an indicator of future performance and current or future trends.

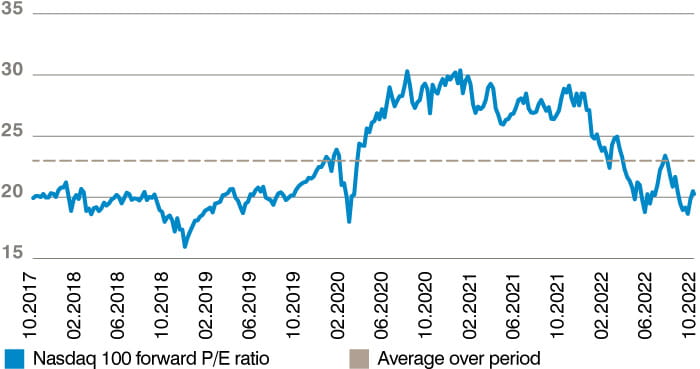

But if the broad US market is now offering reasonable value, the epicentre of inflation and interest rate uncertainty – US large cap technology – appears to be offering even more on some measures. Today the forward price-to-earnings ratio of the Nasdaq 100 index stands at 20x, below the average 23x valuation of the last five tumultuous years and around the level of valuation offered by the index just before the pandemic rally of spring 2020. For investors not already exposed to growth-style US tech stocks this represents an extraordinary opportunity to own the US hub of technological and productivity innovation at valuations that pre-date the huge rally of 2020 and 2021.

Figure 2: US Tech Growth stocks are offering…Value

Source: Bloomberg, as at 31 October 2022. Past performance is not an indicator of future performance and current or future trends.

Turning to bonds, the 10-year US Treasury note offers a yield of 4.0% as of the end of October 2022. US Treasury yields represent the sum of two core predictions by the holder – the long-term nominal GDP growth rate and the long-term inflation rate. As such, 4.0% seems slightly low. The International Monetary Fund’s latest World Economic Outlook suggests that US GDP growth will alone be around 2% by 2027 and, assuming inflation remains around 3% for the next decade, a yield of 5% would not be unreasonable. An adjustment to the ‘right’ yield will of course result in a capital loss for investors. However, the synthetic price-to-earnings ratio of the 10-year US Treasury paints a picture of fairer value. It can be derived by dividing the bond’s ‘price’ (100) by its ‘earnings’ (4.0) to get an equivalent price-to-earnings ratio of 25x. So the overall picture for US Treasury valuations is somewhat mixed. In the world of high yield corporate (‘junk’) bonds, things are unequivocally expensive. The yield in excess of the risk-free rate has traditionally provided a reasonable picture of future returns for this asset class and as of the end of October, the spread for US high yield, as measured by Bloomberg, stands at 4.6%. Based on historical trends, this suggests a somewhat mediocre future five-year return of around 4%, far less than equities might deliver according to the Shiller CAPE. High yield bonds have simply not become sufficiently cheap given the looming recession – and therefore the default risks companies face.

With equities the clear valuation ‘winner’, the next question for investors is what will be the catalyst for this value to be realised? Today, that catalyst surely looks like a peak in interest rates, which affect the net present values of all assets including of course equities. This peak may come sooner than expected. Already, raising rates to deal with inflation is causing increasing moral discomfort given the significant human costs involved. Finnish Prime Minister Sanna Marin recently Tweeted that “There is something seriously wrong with the prevailing ideas of monetary policy when central banks protect their credibility by driving economies into recession”. At the same time, the Bank of Canada’s recent smaller-than-expected rate rise was at least in part a result of awareness of the darkening economic outlook. Crucially, the US Federal Reserve’s (Fed) rate-setting committee is also starting to have doubts about relentless rate rises. Fed Vice Chairwoman Lael Brainard in an important October speech set out a case for pausing rates outright at some point. Perhaps even more likely to stop central bankers in their tracks is the troubling evidence that rate rises are not really curbing inflation. In countries like Chile even aggressive rate hikes appear to have had little effect on price rises. Rates there now stand at a staggering 11.25% while inflation is still running at nearly 14% and wage growth continues to accelerate. At some point Einstein’s definition of madness surely comes to mind. All of this suggests that a profound re-think of deploying rates to deal with complex supply-driven inflation spikes is both appropriate and increasingly likely.

Valuations should be uppermost in the minds of all investors but especially those considering when to make fresh allocations. 2022’s ‘Everything Sell-Off’ has revealed a nuanced picture across different asset classes. Optimism rather than dread is the appropriate sentiment for equity investors, while scepticism is better reserved for bond investors, particularly in corporate credit which is simply not providing sufficient premium for the upcoming risk of economic slowdown. Consistent market timing is of course virtually impossible but equity investors in general – and tech investors in particular – may not have long to wait before a re-rating which vindicates their patience and time horizon. Blinkered monetary policy tightening to deal with today’s inflation spike is raising serious questions as the vanguard of hawkish central banks see limited impact on prices but plenty of impact on ordinary people. As the emphasis shifts and orthodoxy is challenged, financial conditions will surely have to loosen and asset prices should re-rate. The clear winners will be those assets which have become historically cheap relative to the cashflows they promise. The time for patience may soon be over.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.