The tourism industry has faced a tough two years but this summer has been much more positive. GAM Investments’ Swetha Ramachandran examines what a return to travel could mean for the luxury sector.

09 November 2022

In 2020, the tourism industry skidded to a halt and over the following two years saw many false starts as the world grappled with the Covid-19 pandemic.

Now, a strong summer 2022 tourism season globally was confirmed by datapoints released by IATA (International Air Transport Association). Data to the end of August confirmed the return of global air traffic at circa 74% of pre-Covid levels. US and European airlines posted the strongest load factors during this period. Similarly, the UNWTO’s (United Nations World Tourism Organization) World Tourism Barometer update showed that through the end of July, international tourist arrivals versus 2019 levels had recovered the most in Europe, the Middle East and the Americas and remain the most suppressed in Asia Pacific – led by the rolling Covid lockdowns and interruptions to human mobility in the region’s largest travel market, China.

According to the latest UNWTO World Tourism Barometer, international tourist arrivals almost tripled in the period January to July 2022 (+172%) compared to the same period of 2021. This means the sector has recovered almost 60% of pre-pandemic levels. The steady recovery reflects strong pent-up demand for international travel as well as the easing or lifting of travel restrictions to date (86 countries had no Covid-19 related restrictions as of 19 September 2022).

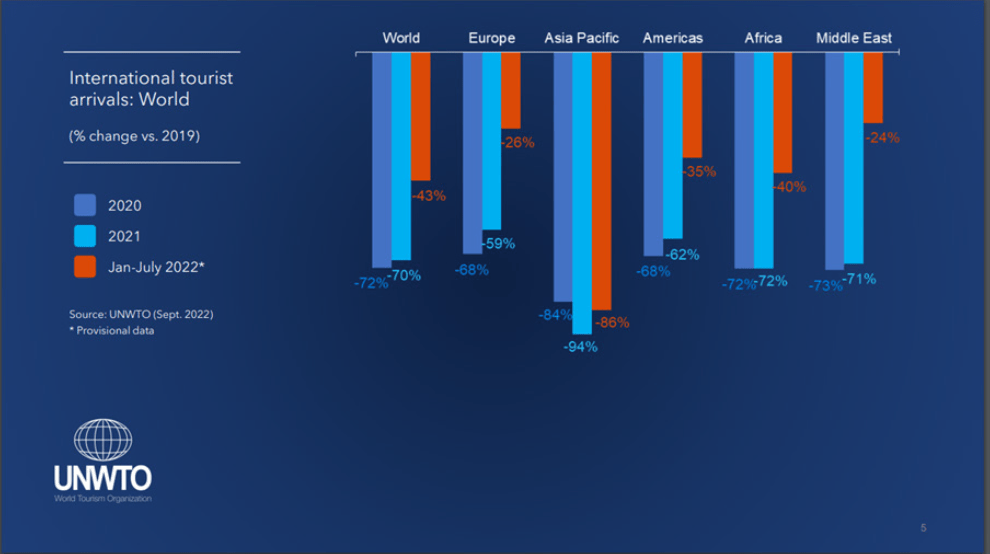

Exhibit 1: Significant recovery in international tourist arrivals versus 2019, globally ex Asia Pacific

Source: UNWTO World Tourism Barometer, September 2022. Past performance is not a reliable indicator of future results or current or future trends.

According to the UNWTO World Tourism Barometer, approximately 474 million tourists were estimated to have travelled internationally over the January to July period, compared to the 175 million in the same months of 2021. An estimated 207 million international arrivals were recorded in June and July 2022 combined, over twice the numbers seen in the same two months last year. These months represent 44% of the total arrivals recorded in the first seven months of 2022. Europe welcomed 309 million of these arrivals, accounting for 65% of the total.

Europe and the Middle East showed the fastest recovery in January-July 2022, with arrivals reaching 74% and 76% of 2019 levels respectively. Europe welcomed almost three times as many international arrivals as in the first seven months of 2021 (+190%), with results boosted by strong intra-European ‘local’ demand as well as, importantly for spend in the region, inbound tourism from the US.

On a scale of 0 to 200, the UNWTO Panel of Tourism Experts rated the period May-August 2022 with a score of 125, equivalent to the bullish expectations expressed by the panel in the May survey for the same four-month period (124).

The impact on luxury equities

Luxury companies have been among the outsized beneficiaries of this summer’s boom in European travel. On the one hand, the local European high-end consumer has lagged their Chinese and US counterparts in staging a spending recovery. If 2020 was the year of Chinese consumers’ ‘revenge spend’ and 2021 the year of US consumers flush with excess savings and ready to splurge, the summer of 2022 appears to have catalysed the re-appearance of European luxury consumers – a characteristic also noted by consultancy Bain in its mid-year update on the global luxury market, which highlighted the steeper recovery curve of the European luxury market.

Higher tourism spend by Americans in Europe has benefited as a result of significant currency volatility, which has led to European prices averaging as much as 30% lower than prices in the US, with the added benefit of VAT refunds, which could increase the price differential on the same stock keeping unit (SKU) to up to 40% in Europe versus the US.

More than halfway through the Q3 earnings season, a common refrain from reporting companies has centred around the boost to sales in the European region from tourists, especially those from the US. Conversely, we have seen some normalisation in spend domestically in the US as more of those luxury dollars are spent while travelling abroad. Overall, the shift in spend is a positive for luxury companies given the high fixed cost base of their European store estates – which carry a fixed rent lease structure versus more variable, turnover-based rents common in China and increasingly in the US. This is likely to positively amplify operating leverage for luxury companies in the third quarter. Moreover, we continue to see further evidence of polarisation and brand bifurcation as tourists splash out on an ‘iconic’ brand or model from a trusted and known ‘top tier’ brand than an up and coming brand. The big are likely to continue getting bigger.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.