Private Shares – An opportunity to participate in the accelerating growth of companies staying private for longer

December 2023

Challenges and opportunities: Click here to read GAM's investment managers' Outlooks for 2024

By investing in later-stage, highly differentiated private companies in areas like artificial intelligence and machine learning, cyber security, robotics, big data and analytics, and fintech, that have typically generated robust operational metrics and often have very strong balance sheets, we believe investors can potentially generate attractive risk-adjusted returns and with far less volatility during their holding period compared to public equities. We continue to see the most significant innovation and disruption happening in the private market which we think, once again, underscores the importance for all investors to have access to the private innovation economy.

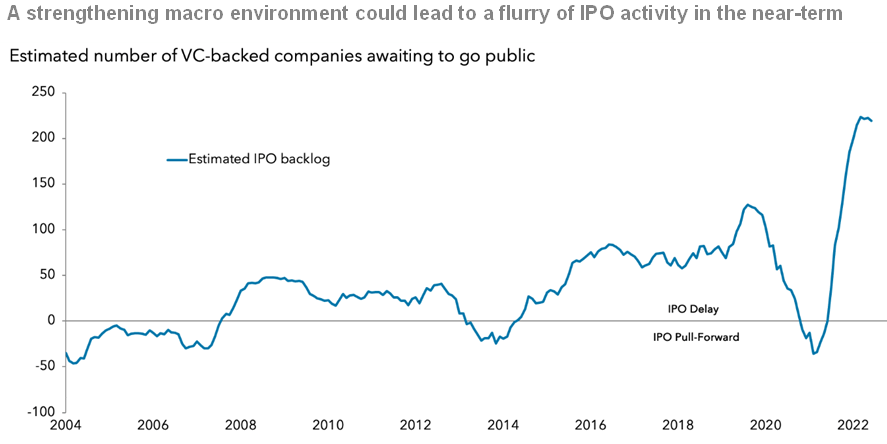

Unprecedented Backlog of VC-Backed Pre-IPO Companies

Source: iCapital as of 6/12/2023

The above chart shows the estimated number of VC-backed companies waiting to go public. It used to be a relatively short journey from founding to listing innovative tech companies. Take Apple (NASDAQ: AAPL) or Adobe (NYSE: ADBE) which both only took four years to list. It is a different story today with companies staying private for longer. Atlassian (NASDAQ: TEAM), for example, took 15 years to list, while Airbnb (NASDAQ: ABNB) took 17 years. Unsurprisingly, this longer lead time to initial public offering (IPO) has seen the number of unicorns [private companies valued at over USD 1 billion] in the private market increase dramatically as they mature into larger operating businesses. As a result, when such companies launch on the public market (or are bought out), it is now typically at a significantly higher value than in the past which means investors unable to access them privately may be missing some of the opportunity to participate in the accelerating growth of these companies in later stages of development.

Venture capital is not traditionally accessible to most investors, bar the biggest institutions and wealthiest investors. It can also come with different risk-return profiles depending on which point of the development cycle you invest in. Usually the accelerated growth phase, which many refer to as late-stage venture and growth equity, offers a more attractive risk-return profile compared to earlier stages.

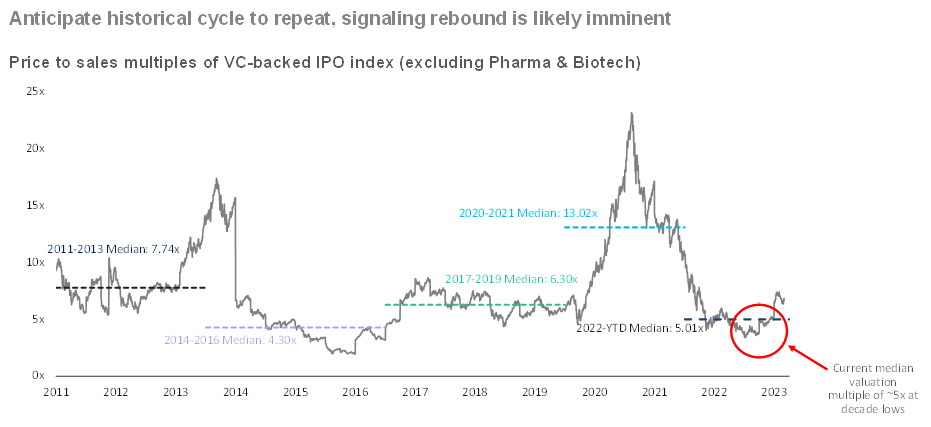

VC-Backed IPO Valuation Multiples at Historic Lows

Source: Pitchbook NVCA Monitor as of 9/30/2023.

Although we never recommend that any investor try to time entry into any asset class, particularly ones that require a longer-term perspective like ours, we cannot think of a better time to be allocating to the late-stage venture and growth space given both the opportunity set and amount of price dislocations in the market. The VC-backed IPO valuation multiples are at historic lows, with the median Price-to-Sales (P/S) ratios of the VC-backed IPO index (excluding pharma and biotech) at decade lows of 5 times. We anticipate that this historical cycle will repeat, and there are signals that a rebound is likely imminent.

While we are seeing multiple signs of sentiment shifting to the positive and expect this trend to continue in 2024, we remain keenly aware that the current macro environment and geopolitical landscape present multiple challenges, which can further impact both valuations and exit activities. However, it is important to understand that historically, investments made during periods of dislocation have generated strong performance in subsequent years largely due to discounted entry points and the ability for investors to negotiate more favourable terms, but investors must be patient, disciplined and share our longer-term perspective in order to benefit.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.