European Equities – We remain positive on the prospects for the European banking sector; market pricing of the stocks has failed to appreciate the sustainable nature of the increase in earnings and return on equity from a return to positive interest rates

December 2023

Challenges and opportunities: Click here to read GAM's investment managers' Outlooks for 2024

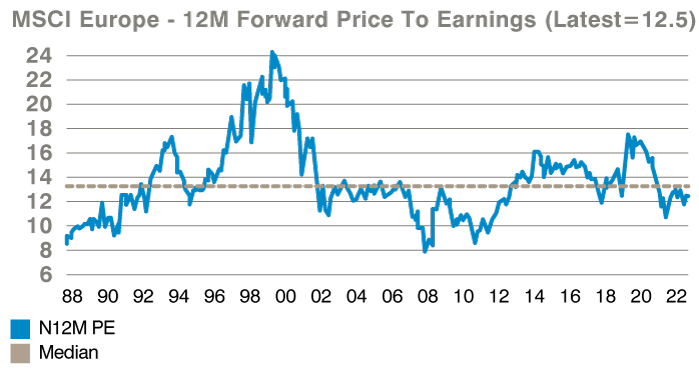

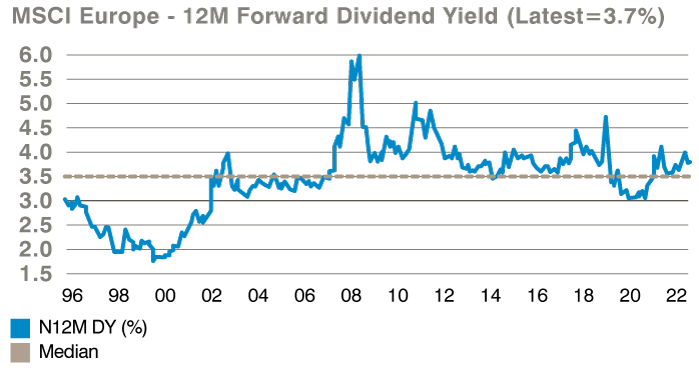

We think the prospects for further accretion in the value of European equities into 2024 are positive. The European equity market (as represented by the MSCI Europe Index) remains attractively valued on 12.5x forward earnings, which is below long-term median values and the expected earnings growth for the next two years is 6% for 2024 and 9% for 20251, respectively. The prospective dividend yield is also very attractive at 3.7%2 (and well above median values) while share buybacks are becoming an increasingly important component of the European market, driven by banks and energy sectors and add about 2% to the dividend yield leading to an overall distribution yield of 5.7%. Despite the negative sentiment around the European economy, it is important to remember that only 42% of the revenues of the MSCI Europe index are derived from western Europe, with most revenues now derived from faster growing parts of the world; this changing exposure ultimately serves to increase the structural growth rate of the asset class. The forward price/earnings multiple of our strategy (a weighted average forward price earnings multiple of the strategy’s holdings) is in line with the MSCI Index illustrating a lack of style bias at the present time, consistent with our style agnostic/style flexible investment process.

European forward valuation multiples I

Source: Morgan Stanley, as at 6 December 2023.

Past performance is not an indicator of future performance and current or future trends.

European forward valuation multiples II

Source: Morgan Stanley, as at 6 December 2023.

Past performance is not an indicator of future performance and current or future trends.

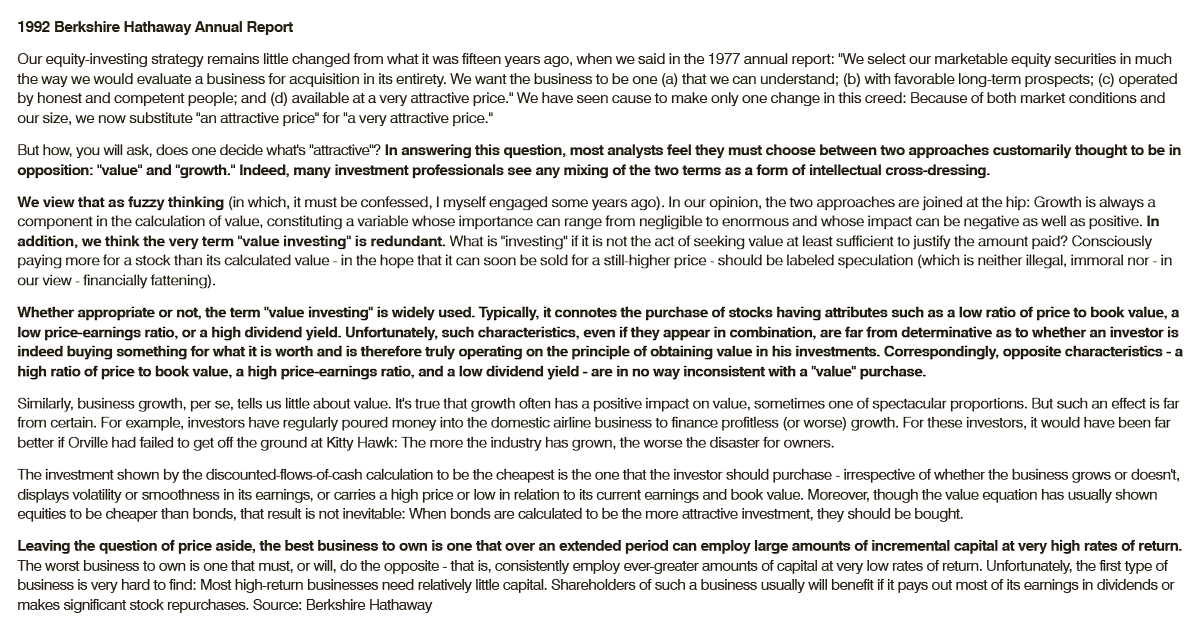

A broad mix of performance drivers over the course of 2023 – despite running a concentrated/focused investment process – is testament to our mantra of driving both stock selection and portfolio construction through taking idiosyncratic risks and avoiding being dragged into the tedious growth versus value box sorting; we think this is the most appropriate way of managing money and generating long-term alpha, and hopefully helps us avoid being stuck in cognitive traps where we have to justify owning expensive stocks, or value traps because of adhesion to a proclaimed style bias. We remind readers of one of our favourite Warren Buffet quotes from the 1992 Berkshire Hathaway Annual Report.

Source: Berkshire Hathaway, as at 31 December 1992.

Source: Berkshire Hathaway, as at 31 December 1992.Looking into 2024 we remain positive on the prospects for the European banking sector; market pricing of the stocks has failed to appreciate the sustainable nature of the increase in earnings/return on equity (ROE) from a return to positive interest rates. We think a return to the extreme interest rates of 2008-2021, which represented a multi-century low in rates, according to the Bank of England, is highly unlikely yet this is what is priced into share prices. As long as interest rates remain above 2% banks can continue to earn attractive ROE, which are well above any conservative estimate of the cost of capital, yet most of the sector still trades at a discount to book value despite returns on tangible equity between 12 and 20% for most stocks; this makes no sense.

The energy sector shares some of the same ‘market characteristics’ as the banks sector with very low valuations relative to history and high cash returns, through dividends and buybacks. We think this may in part be due to many investors refusing to invest in this sector – either because their mandate precludes it or because they have forgotten, or do not know how to analyse the sector as with banks (all very poor excuses). We have articulated the view many times over the past three years that we expect the oil price to remain in a higher price range over the next decade given a significant reduction in global capital investment in hydrocarbon extraction into a (still) rising demand picture, driven by developing/non-Organisation for Economic Co-operation and Development (OECD) countries desiring the same middle-class living standards we enjoy in the OECD. We would add to this that shortages and price inefficiencies are likely to occur across the energy spectrum due to insufficient capital investment and this will offer profit opportunities in a whole range of areas across refining, trading, liquefied natural gas (LNG), marketing and retail operations – indeed one could not invent a better set of badly thought through and woefully implemented public energy policies than those we have at present across Europe, that provide for attractive profit making opportunities for energy companies and attractive returns on capital employed. It is also critical to remind readers that we see a very large role for European integrated energy companies in the energy transition and indeed believe that the energy transition will not be possible with the engineering expertise and financial clout of European energy companies; European companies are active across activities such as solar and wind power deployment (onshore and offshore), green and blue hydrogen, electric vehicle (EV) charging roll-out, biofuels, sustainable aviation fuel, carbon capture and storage, and we will continue to support them in their efforts to decarbonise our societies.

Outside of banks and energy we retain significant exposure to parts of the market benefiting from strong structural growth drivers, where we strive for our holdings to be best in class globally and where the equity is attractively/appropriately valued. We believe the most interesting such area is semiconductor and semiconductor capex-exposed technology companies encompassing our holdings in Infineon, STM, ASM International, BE Semiconductor and Atlas Copco. The single biggest drivers of Infineon and STM is the automotive sector where the transition to EV and the growth of safety and autonomous driving will dramatically increase the semiconductor content per car (by a multiple) such that increased penetration of these technologies power secular growth. What we particularly like about automotive semiconductors (across the range of automotive applications) is that once designed into a vehicle there is typically strong persistence of demand as automakers tend not to change semiconductor components absent a major redesign of the vehicle; over and beyond this, we see very strong growth from broader electrification trends such as renewables and the explosive growth in data centre power requirements. It seems hard to believe that Infineon and STM trade at close to decade low valuations given the strong position they enjoy in their respective segments, and the much higher levels of valuations US peers trade on in addition to the strong structural growth. Our semiconductor capex stocks, ASM International and BE Semiconductor have both experienced extraordinary share price appreciation in 2023 and are trading at multiples closer to the top of their historic ranges, which has encouraged some profit taking on our part, but we remain attracted by the very powerful structural growth drivers requiring semiconductor ‘shrink’ beyond lithography.

Other areas where we see an attractive combination of valuation, structural growth and decent returns are in industries that we expect to see strong impetus from decarbonisation and the transition to net zero. Stocks exposed to electrification where a 2-3x increase in electricity generation transmission and distribution is required by 2050 include Prysmian, Schneider (and of course Infineon and STM); stocks exposed to the building envelope with a need for stricter new build standards on thermal efficiency and new build include Kingspan and Saint Gobain; while stocks exposed to green and blue hydrogen include Linde, Atlas Copco as well, of course, as our energy holdings. The transition to net zero is going to require a monumental pick up in physical capital expenditure – far higher than politicians have explained to their electorates – and this will be a strong demand driver for many of our portfolio companies with the right exposure.

Beyond the above exposures, driven by identifiable structural growth drivers, we have several large exposures with strong idiosyncratic drivers. Such stocks include Ryanair, Volvo Trucks, Novo Nordisk and Inditex. The key driver of Ryanair is the juxtaposition of a very strong market position in short- haul intra-European aviation, combined with well controlled and established costs and a strong delivery schedule of new planes at a time when the industry is supply constrained and customer demand is normalising post- Covid; the stock trades on an exceptionally low valuation and is about to become very cash generative driven by rising fares and falling capital intensiveness. The company also leads the aviation sector in ‘greening’, having very low carbon emissions per passenger KM and a clear strategy to deploy sustainable aviation fuel. Novo Nordisk continues to power forward on the back of explosive demand for its transformative weight loss drugs and excellent results from clinical trials focused on cardiovascular and kidney disease risks. We are big bulls on the long-term potential of these drugs to improve human health but the path will not be a linear one and valuations are elevated versus history.

1 Source: Bloomberg, as at 6 December 2023

2Source: Bloomberg, as at 6 December 2023

2Source: Bloomberg, as at 6 December 2023

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

Specific investments described herein do not represent all investment decisions made by GAM. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets (DM) countries in Europe. With 428 constituents, the index covers approximately 85% of the free float-adjusted market capitalisation across the European Developed Markets equity universe. Investors cannot invest directly in indices. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with the Funds. Therefore, comparisons to indices have limitations.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

Specific investments described herein do not represent all investment decisions made by GAM. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets (DM) countries in Europe. With 428 constituents, the index covers approximately 85% of the free float-adjusted market capitalisation across the European Developed Markets equity universe. Investors cannot invest directly in indices. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with the Funds. Therefore, comparisons to indices have limitations.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.