Flavio Cereda, Investment Manager, Luxury Equities, explores the post-Covid transformations in the luxury sector and how the top brands have adapted. He also discusses the future implications and opportunities.

13 November 2023

The luxury sector is one of the most dynamic and resilient sectors in the world. It has always overcome challenges and crises and emerged stronger and more profitable. However, the Covid-19 pandemic has brought unprecedented changes and disruptions to the sector, forcing it to adapt and transform to survive and thrive. The luxury spending in China, the most important and influential market for luxury brands, has spiked and is now normalising. Luxury brands have also experienced a polarisation effect, where the stronger brands have gained significant market share at the expense of the weaker ones.

The rise of Asia and the decline of Europe in the luxury market

The luxury market has shifted dramatically in geography and nationality from 2019 to 2023. China has doubled its share of the sector from 14% to 28%, while Asia as a whole has increased its share from 28% to 47%, making it the most important region for luxury brands. Europe, on the other hand, has seen its share drop from 49% to 30%, mainly due to the decline in tourism and travel caused by Covid-19 and the stricter border controls by the Chinese authorities

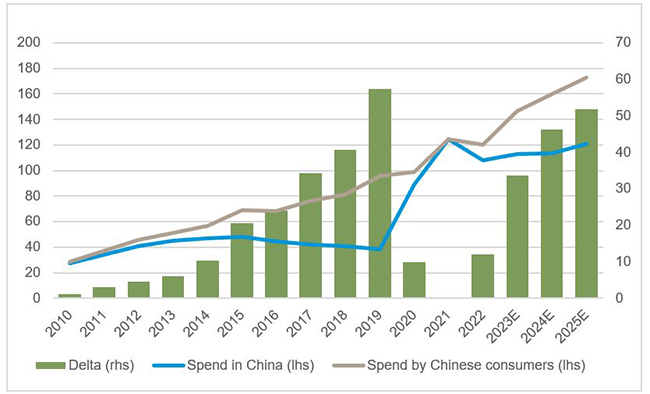

Chinese consumers are the key drivers of the luxury sector, accounting for an estimated 36% to 38% of global sales this year, compared to 34% in 2019. According to more conservative forecasts from Bain, Chinese consumers should further strengthen their status as the dominant nationality for luxury, growing to represent 38%-40% of global purchases by 2030.1 However, they are now buying more luxury goods locally, as it is becoming more expensive and difficult to travel abroad. In 2019, Chinese consumers accounted for 34% of luxury sales but China geographically only accounted for 14%. This is because they spent in other countries, especially in Europe, Japan, South Korea and Hawaii. As the trend shifts towards a more domestic focus, it is estimated that China geographically will account for 28% of global luxury sales in 2023.

The luxury sector is facing a new reality, where Asia matters more than ever and Europe matters less and less. According to the data from Statista, Asian consumers, including Chinese and other nationalities, account for about 55% of the luxury sector this year, while European consumers only account for 15%. Luxury brands need to have the right stores, the right digital presence, the right pricing, the right social media presence, and the right ambassadors in Asia, especially in China, to succeed in the market.

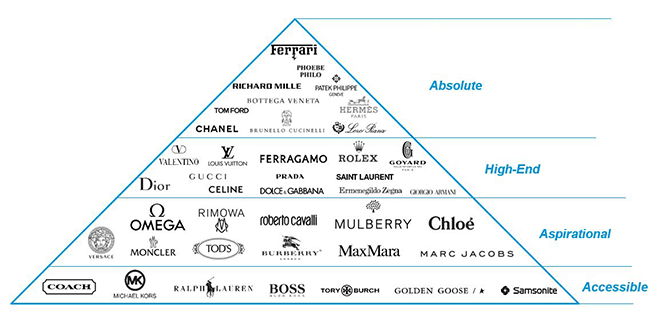

The luxury pyramid: how polarisation creates winners and losers

The luxury sector has changed a lot since the 2007-2008 global financial crisis. It is now bigger, more profitable, and more resilient, and as already stated more dependent on the Asian market, especially Chinese consumers, who are the most important and influential customers for luxury brands.

Source: GAM as at October 2023. The views are those of the manager and are subject to change The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Logos are trademarks of their respective owners and are used for illustrative purposes and should not be construed as an endorsement or sponsorship of GAM.

We have categorised the luxury sector into what we call the ‘luxury pyramid’: Absolute, High-end, Aspirational and Accessible. The higher the category, the better the quality, the margin, the demand and the loyalty.

LVMH, Hermès and Kering are three examples of contrasting performances in luxury. LVMH and Hermès have both grown remarkably from 2019 to today23, thanks to their brands’ absolute and high-end positioning in the luxury pyramid. Kering, on the other hand, has been underperforming for a while, mainly due to the disappointing performance of Gucci, which accounted for 80% of its profits in 2021.45

The luxury sector is undergoing a major transformation, and we believe the brands that are at the top of the pyramid will be the ones that will thrive in the post-Covid era. They have the quality, the reputation and the resilience that make them more attractive and more defensive than the lower-end brands. They have been able to adapt to the changing preferences and behaviours of Asian consumers, especially the Chinese. They have also been able to innovate and diversify their products and services, while maintaining their exclusivity and craftsmanship.

The MEDALS strategy: how luxury brands are reaching out to new customers

The MEDALS strategy, which stands for music, entertainment, digital, arts, lifestyle and sports, is a way to understand what the best luxury brands are doing to outperform. Brands can broaden their reach and interact with consumers in a variety of ways, such as sponsoring concerts, partnering with athletes or supporting artists. By focusing on these different categories, they are reaching out to new, younger customers. Generation Z will soon be the biggest buyers of luxury, but they need to be aware of the brand first. The MEDALS strategy increases their awareness, interaction and engagement with luxury at an earlier stage. What these brands are doing is locking in these customers early and building up their future customers, aiming to build their growth potential as a result. This is what we call the premiumisation of everything; luxury brands are getting involved in categories and areas where they would never have been involved 10 years ago, and these have the potential to be super accretive revenue opportunities.

The future of the luxury sector: growth, margin and innovation

Chart 1: Chinese spend dynamics since 2010

Source: Bain, GAM as at 31 October 2023. The views are those of the managers and are subject to change. GAM has not independently verified the information from other sources and GAM gives no assurance, expressed or implied, as to whether such information is accurate, true or complete.

Past performance is not an indicator of future performance and current or future trends. There is no guarantee forecasts will be realised. For illustrative purposes only.

The luxury sector is facing a new reality in the post-Covid era, where brands’ growth, margins and innovation will determine their success and their survival. Luxury spending in China, the most important and influential market for luxury brands, is expected to grow by 5% next year. Luxury brands will have to work harder to attract and retain these Chinese customers, who have shown a strong appetite and a high loyalty for luxury goods, but who also have changing preferences and behaviours.

The margin boom that we witnessed in the last three years is all but over. The key here is to grow revenues and increase market share further, which should enable them to maintain their margins. The stronger brands, such as Louis Vuitton, Dior, Hermès and Chanel, could benefit more from the growth in the luxury sector, as they have the edge in quality, brand identity, customer experience and innovation.

1 https://www.bain.com/insights/renaissance-in-uncertainty-luxury-builds-on-its-rebound/

2https://r.lvmh-static.com/uploads/2023/10/lvmh-2023-third-quarter-revenue.pdf

3https://assets-finance.hermes.com/s3fs-public/node/pdf_file/2023-10/1698077038/hermes_20231024_ca3t_en.pdf

4https://www.reuters.com/business/retail-consumer/kering-sales-down-9-luxury-slowdown-weighs-turnaround-efforts-2023-10-24/

5https://www.reuters.com/business/retail-consumer/gucci-stumbles-kering-gears-up-brands-100th-year-2021-02-17/

2https://r.lvmh-static.com/uploads/2023/10/lvmh-2023-third-quarter-revenue.pdf

3https://assets-finance.hermes.com/s3fs-public/node/pdf_file/2023-10/1698077038/hermes_20231024_ca3t_en.pdf

4https://www.reuters.com/business/retail-consumer/kering-sales-down-9-luxury-slowdown-weighs-turnaround-efforts-2023-10-24/

5https://www.reuters.com/business/retail-consumer/gucci-stumbles-kering-gears-up-brands-100th-year-2021-02-17/

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Past results are not necessarily indicative of future results. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Past results are not necessarily indicative of future results. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.