GAM Explains: The IPCC Mitigation of Climate Change Report

05 August 2022

With the global spotlight fixed on the Russia-Ukraine war, the latest report from the UN’s International Panel on Climate Change (IPCC) did not make many headlines, yet its findings are momentous. The report offers an alarming depiction of the scale and scope of the action still needed to tackle the climate crisis.

The United Nation’s International Panel on Climate Change published its Working Group III Sixth Assessment report (AR6) in April 2022. At almost 3000 pages, it brought together a significant amount of research from world-leading climate scientists across 195 countries, tasked with assessing the efforts made in mitigating climate change; assessing the implications the world will face on its current warming trajectory; and conveying what is needed to meet long-term climate goals.

The report is the third in a three-part assessment. Its predecessors were ‘The physical science basis’ (Working Group I), published in August 2021, which concluded that Earth’s warming is unequivocally human-induced. The second part, ‘Impacts, adaptation and vulnerability’, was issued in February 2022 and found that no place on Earth would escape the impacts of global warming.

Climate change is a systemic risk affecting all sectors and markets. The mitigation report demonstrates both the extent and speed with which investments that seem sound now can become much riskier. This is not limited to obvious sectors such as energy or transport, but rather affects all parts of the global economy.

The report outlines how far behind the financial sector is in reaching the funding levels needed to meet the targets set out in the Paris Agreement, and the need for investors to substantially increase investment in renewable energy and other low-carbon solutions.

This transition will be the biggest economic transformation since the Industrial Revolution and the findings of the report suggest that capital markets must be innovative and bold in their support for low carbon activities.

How investors choose to invest in the coming years and whether they can encourage the companies they invest in to adopt robust Paris-aligned strategies are likely to be definitive for the future of the planet, as well as for their own portfolio returns.

At GAM we are already investing in opportunities from green hydrogen to green housing, and engaging with our portfolio companies to actively manage their climate risk. Last year we exited our investment in a large German utility company in large part due to an inadequate plan to reduce its carbon footprint.

Our Sustainable Climate Bond is one of the first green bonds to focus on European financial issuers. European banks dominate the European corporate financing landscape and therefore have a pivotal role in driving sustainable growth. In its first year the projects financed by the green bonds in the portfolio helped avoid 1,580 tons of CO2e – equivalent to driving a car more than 200 times around the Earth. They also helped install 2.8MW of renewable energy capacity and to financing around 1500m 2 of green buildings.1

- We are on track for 3°C without immediate and deep emission cuts that peak by 2025

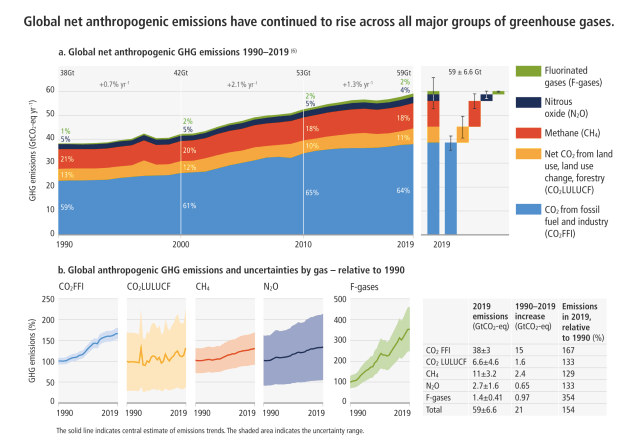

The IPCC research demonstrates that during the period 2010-2019 annual emissions continued to grow, though at a lower rate than in the previous decade, with 59 billion tonnes of carbon dioxide equivalent (C02e) added to the atmosphere in 2019. To put this in perspective, globally we emitted the equivalent weight of 121 million jumbo jets in 2019 alone.

The IPCC findings show that the climate crisis is about much more than just fossil fuels. The report assesses activities across the whole economy, from construction to cattle, retail to real estate and fashion to forestry. For example, take the livestock sector – if cattle were a country they would be the world’s third highest emitter of greenhouse gases.

Furthermore, the IPCC finds that nations and non-state actors are falling short on net-zero targets. Even with current climate pledges, the world is on track to reach a 3˚C2, irreversible, warming scenario. The authors of the research found that in order to limit temperature rises to 1.5˚C, emissions need to peak before 2025 and reduce by 43% by 2030, reaching net zero by 2050.

Figure 1: Global net anthropogenic GHG emissions (GtCO2-eq yr-1) 1990–2019

Source: IPCC (2022) Figure SPM.1

- Incentivise action through market and regulatory instruments

The report points to the power of economic and political tools in driving action. Decision makers can generate a reduction in fossil fuels by, for example, policies that introduce carbon pricing mechanisms or those that remove fossil fuel subsidies. Financial incentives can also be used to stimulate positive action, such as boosting carbon-cutting technological innovation. Evidence has shown that mitigation policies have led to a reduction in greenhouse gas emissions3, yet more regulation and financial opportunities are needed for a sustainable transition.

In the financial sector, regulation is taking place in the form of risk management and disclosure, such as the rollout of the Task Force on Climate-Related Financial Disclosures and the recently proposed US SEC rules, which form the basis for how markets can better manage climate risk. These developments help to hold companies and financial markets to account, encouraging positive action among corporates.

It is clear from the report, however, that commitments from financial institutions must rapidly turn into action at portfolio level.

- Much more finance is needed to curb global warming

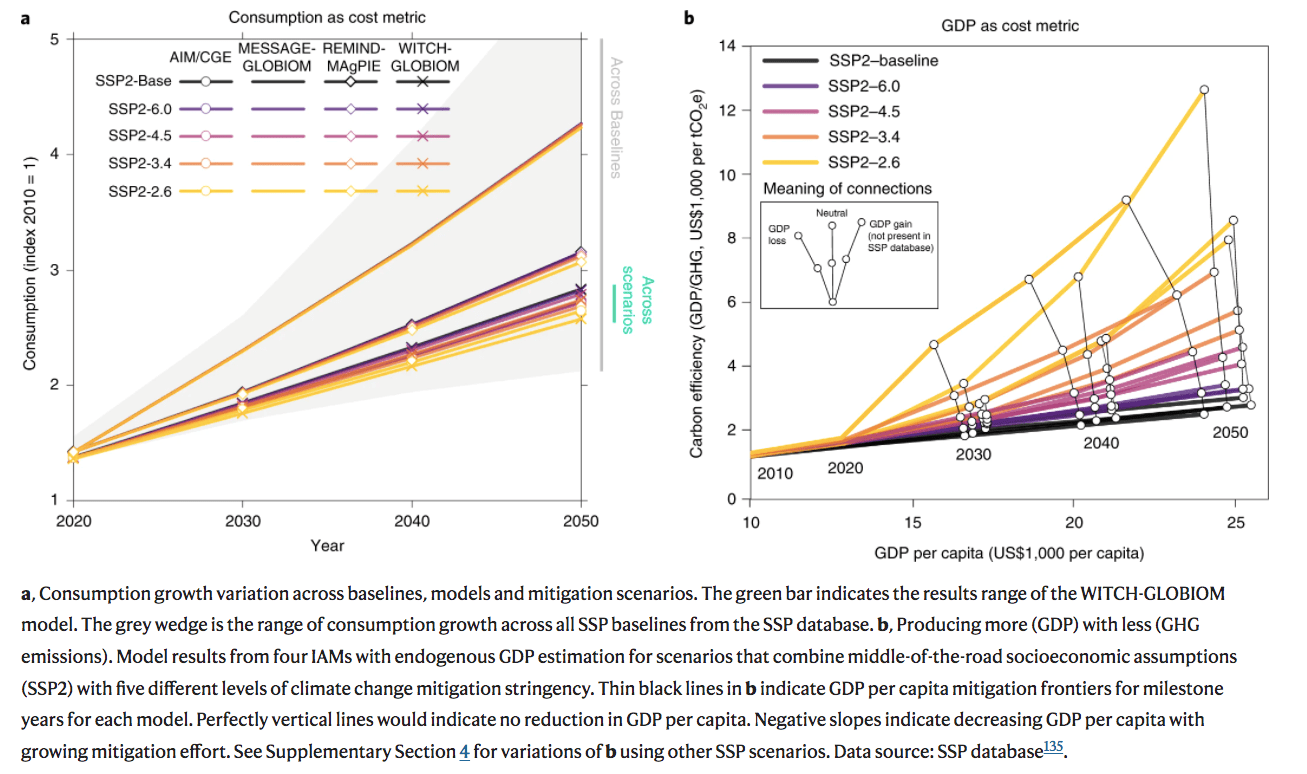

In short, acting now is critical but this action requires funding, with IPCC warning that climate finance is currently three to six times lower4 than what is needed to keep warming below 2˚C.

Total climate finance for mitigation and adaptation is estimated at up to USD 385 billion per year, the equivalent of delivering the US Covid-19 rescue plan every year.

The costs of inaction will, however, be greater still. A study by consultancy firm Deloitte estimated that the cost of inaction on the US economy would be USD 14 trillion over 50 years. Moreover, research shows that capital expenditure on climate mitigation leads to growth across many sectors of the economy. Investors must scale up funding to support deep emission cuts and spark innovation for clean technologies.

Figure 2: Mitigation costs in a growing economy

Source: Köberle et al. (2021)

A Synthesis Report is due to be published in September later this year. This will integrate the three latest Working Group reports, as well as the most recent IPCC Special Reports on Global Warming of 1.5°C, Climate Change and Land, and The Ocean and Cryosphere in a Changing Climate.

COP delegates recently convened to consider the impacts of the IPCC’s findings from the Working Group II paper and how to ensure science is at the forefront of the global response at the climate conference in Egypt later this year. We will be closely watching to see how these discussions evolve and incorporate the findings of the latest crucial mitigation report.

To learn more about the findings of the WGIII IPCC, the full report is available to download here.

For more information about sustainability at GAM Investments, please click here.

For more insights from GAM, please visit ‘Our Thinking’ page here.

1 As calculated by Carbone 4 based on the portfolio as of year-end 2021. More information available here

2IPCC, AR6, WGIII, Full Report, 2403

3IPCC, AR6, WGIII, Full Report, 60

4IPCC, AR6, WGIII, Full Report, 185

2IPCC, AR6, WGIII, Full Report, 2403

3IPCC, AR6, WGIII, Full Report, 60

4IPCC, AR6, WGIII, Full Report, 185

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.