Earlier this month, Federal Reserve (Fed) Governor Jerome Powell said that US interest rates may need to rise by more than is currently priced by the market. In contrast, Bank of England Governor Andrew Bailey was explicit in stating that official interest rates in the UK were unlikely to rise as much as the market was expecting – despite, in his words, perhaps the largest upside risks to inflation in the Monetary Policy Committee’s (MPC) history.

08 November 2022

GAM Investments’ Adrian Owens considers whether the UK and US economies are really moving in such different directions and if the inflation outlook is markedly better in the UK.

UK inflation higher than the US

On the surface the UK has a bigger inflation problem with latest headline inflation at 10.1% year-on-year versus 8.2% in the US. Looking specifically at UK RPI inflation, which sits at 12.4%, exacerbates this differential. If we focus on core inflation, however, the UK and the US are more aligned, with the UK at 6.4% and the US at 6.6%, or 5.2% on the Fed’s preferred core personal core expenditures (PCE) deflator.

US Federal Reserve has out hiked the Bank of England

But central bankers are looking to the future and how current policy is likely to impact future inflation. In terms of action to date, the Fed has done more, having hiked rates by 375 bps while the Bank of England (BoE) has raised rates by 290 bps. Real 10-year yields in the US are 1.8% while real yields in the UK remain negative (real yields based off 10-year inflation-linked bonds). Further, sterling, which is key for an open economy like the UK, has performed very differently to the US dollar. According to JP Morgan’s broad effective exchange rate, so far this year sterling is down 5.5% while the US dollar has strengthened by 12.3%. As if monetary conditions were not already tightening at a much slower pace in the UK than the US, the UK’s quantitative tightening programme has also been delayed with its first gilt sale only taking place on the first of this month.

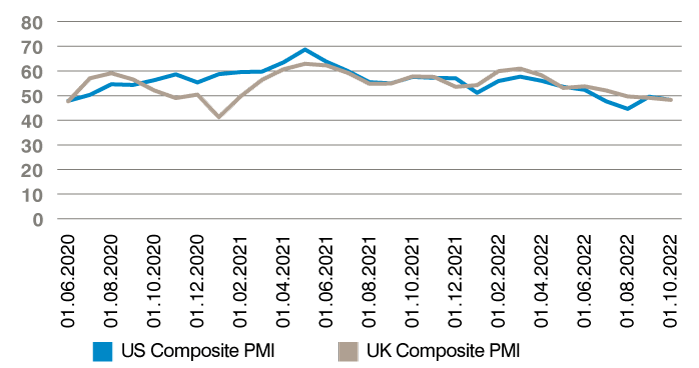

US and UK growth dynamics

At the BoE press conference, which followed the latest rate decision, the Governor was asked directly by a journalist from CNBC why the BoE was behaving so differently from the Fed. Bailey deferred to Deputy Governor Ben Broadbent who emphasised the different growth outlooks, drawing particular attention to the latest PMI data. Broadbent said that the US outlook, based on these indicators, was far better than the UK’s. He stated that the PMIs in the UK and the US were 58 and 57, respectively, at the beginning of the year but the UK was now closer to 47, while the US was much higher at 58. Looking at the latest data, we can see that the US PMI is in reality 48.2 (S&P Global US Composite PMI) - exactly the same as the latest reading for the UK. The deterioration of the UK and US has, on this basis, been in line.

Figure 1: US and UK composite PMIs – a similar path

Source: S&P Global, as at 31 October 2022.

For medium term inflation, growth relative to potential is key

However, in thinking about inflation and the implications for monetary policy, it would have been more informative if Broadbent had talked about growth relative to trend - or relative to the rate of growth at which the economy can expand without creating inflation. There is much uncertainty about where exactly trend growth is but what we can say with some confidence is that in both the US and UK it has been declining over recent years. Various estimates suggest US trend growth was around 3% in the 1980s and is probably closer to 1-2% today. The UK, in contrast, is likely witnessing a trend growth rate somewhere between zero and 1% (which also calls into question former UK Prime Minister Liz Truss’ claim that she wanted to see UK growth at 2.5% at a time of high inflation). We would not be surprised to find that it is currently much closer to zero or negative. Why? As the Office of Budget Responsibility (OBR) highlights, the key determinants are productivity, population growth and hours worked. Evidence suggests that UK productivity remains very weak, labour market participation is low and as Bailey highlighted, inactivity has been on a rising trend.

So, the relative growth outlooks in the US and UK, adjusted for their respective potential growth rates, may not be quite as different as Broadbent implied. In fairness, he also highlighted the impact of the war in Ukraine which has resulted in a much larger shock to UK energy prices than seen in the US. However, this is a double-edged sword, not only affecting growth, but also likely to have a negative impact on the trade-off between UK growth and inflation, implying higher inflation for a given level of growth than would have occurred prior to the war.

In summary then, the US has seen more monetary tightening coming from rates, currency and quantitative tightening than the UK. The growth differences, relative to potential, may not be as large as the BoE suggests yet the MPC has argued that an unchanged rate path is more likely to get inflation back to target than current market pricing! In contrast Chairman Powell at the Fed believes that the peak in interest rates will be higher and stay higher for longer. We are more convinced by the arguments presented by the Fed and do not think that the UK is in such a different position that the BoE will be able to go its own way. Afterall, if UK rates diverge too much from the US, we believe sterling is likely to be impacted, adding further to the already troubling inflation dynamic.

In our view, Bailey and team do not appear to have the appetite to tackle inflation purely through tighter monetary policy. The one thing they do have on their side that may differentiate the UK from the US could be future fiscal policy. The Bank of England bailed out former Prime Minister Liz Truss. Perhaps the government of Prime Minister Rishi Sunak and Chancellor Jeremy Hunt can bail out an overly dovish bank.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. There is no guarantee that forecasts will be realised.