Luxury Brands – Stock picking in 2024 will be more important than at any time since 2016

December 2023

Challenges and opportunities: Click here to read GAM's investment managers' Outlooks for 2024.

Q3 results validate process of growth ‘normalisation’, albeit at different speeds

Once the post-Covid China reopening trade started to fade, and US comparable metrics started to look very tough, the trend towards a more sustainable rate of growth became evident, and as you can probably date this to the start of the holiday season, it was in the Q3 or June-September prints that this became obvious. While relative underperformance started earlier (channel checks, credit card data, post-H1 conversations with management) – effectively in mid-summer – results season unequivocally highlighted this. 2023 was a year of two halves: H1 starting very buoyant and maintaining momentum in Q2, with H2 more challenged on a year-on-year basis and a return to normal growth dynamics which we think will also be evident in H1-24. What we are likely to witness once more is a flight to quality, with the stronger brands appearing to prove their resilience yet again with the upper end of the ‘Luxury Pyramid’ benefiting from more affluent and loyal customers, a less volatile demand pattern and significant pricing power as demand/supply imbalance remains skewed in its favour.

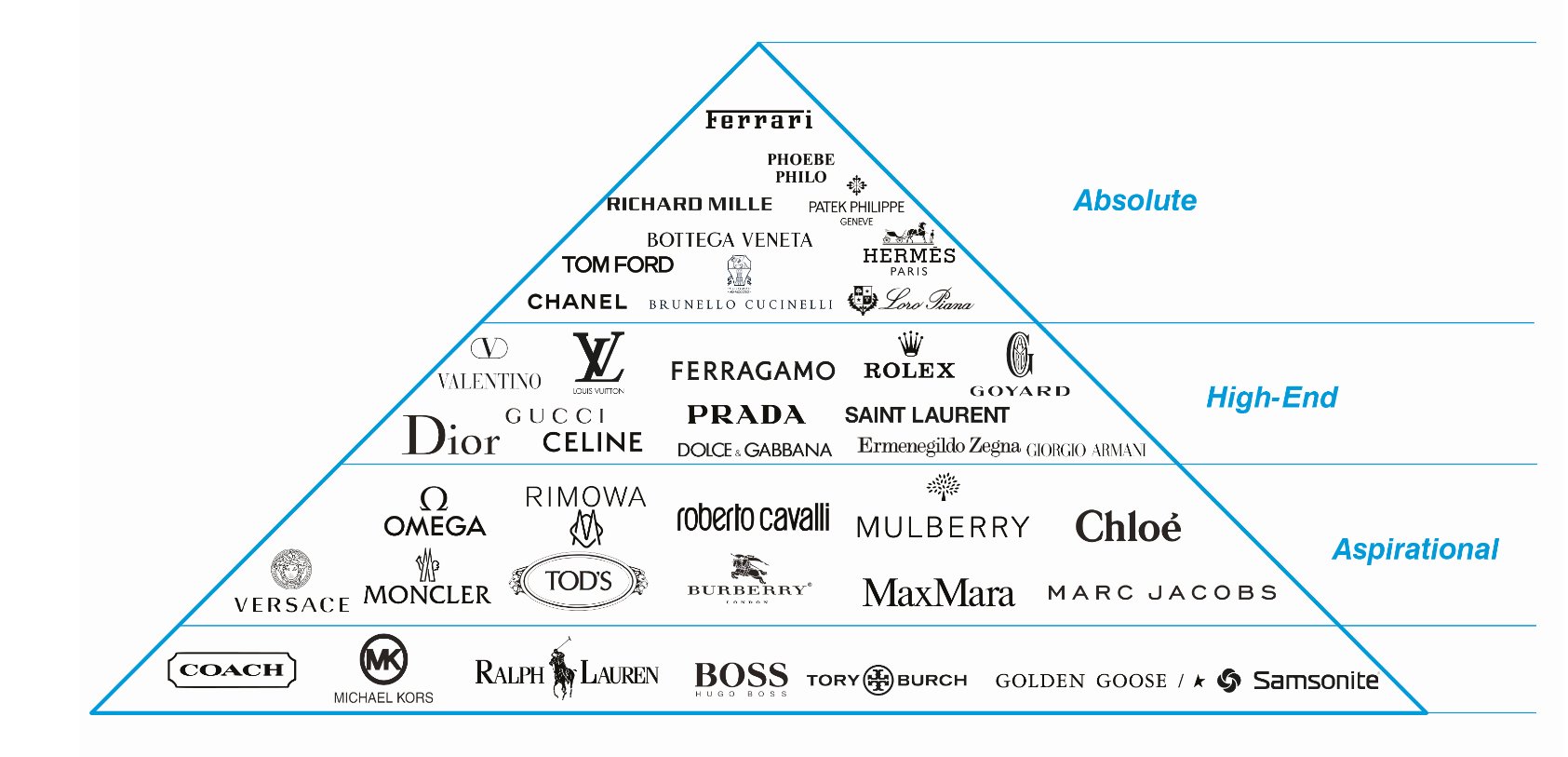

Luxury pyramid: Life's better at the top

Source: GAM as at October 2023. The views are those of the manager and are subject to change The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Logos are trademarks of their respective owners and are used for illustrative purposes and should not be construed as an endorsement or sponsorship of GAM.

Why the deceleration and is it a good thing?

We have to put current trends in context. If we track performance over the longest possible credible period, ie back to 1995, we see the sector growing at a Compound Annual Growth Rate (CAGR) of 6.5% which is a remarkable number in that it implies growth from EUR 66 billion to EUR 343 billion last year. The CAGR since the Global Financial Crisis or from 2010 is 6.4%, delivering further evidence that a mid-single digit metric is not only sustainable but very credible. The sector plunged 22% in 2020 as is known, but fully recovered and more in 2021 when the total value exceeded 2019. And herein lies the challenge: post-Covid recovery, set at different times for different geographies, was abnormally strong, delivering +29% in 2021 and +21% in 2022. These metrics are neither sustainable nor healthy in our view, although they do underline the never-ending appetite for the space amongst consumers globally. What is commonly referred to ‘normalisation’, or a +6-7% yearly growth, is inevitable and significantly more resilient than elsewhere. So yes, it is a good thing as 20%+ growth had blinded the market to the most important of considerations: sustainability. We currently forecast 9-10% growth for the sector in 2023, dropping to 5% in 2024 and 6-8% in 2025.

Is the sector in good shape?

Absolutely. Let us look at it from the point of view of both the consumer and the brands. The consumer of luxury has been increasingly Asian for a number of years, with the US cohort holding its own whereas the European buyer is increasingly less relevant. We believe Asians now account for well over 50% of total spend or similar to 2019 again,only in the context of a sector that is a third bigger. The well-known drivers here, especially in China, such as demographics, growth of the middle class and the importance of social status, continue to deliver an insatiable appetite for luxury further lifted by post-Covid’s travel preference of the Chinese to stay within Asia. The US buyer historically always under indexed in luxury but has recently increased from low- to mid-20s as there has been more interest in the sector after 2020, driven not only by a return to travel and the quest for experiences, but also by the success of the better brands to significantly broaden their reach across categories and trigger a much greater response from younger consumers through involvement in the likes of sports, music and entertainment. The US buyer travelled extensively to Europe in 2022-23 alongside Asians (less so Chinese) and Middle East consumers, hence why Europe is much more relevant for luxury than the Europeans, and will stay this way. The better brands are significantly bigger, much more profitable and better capitalised than perhaps they ever were, leaving them in a strong position to manage any possible short-term volatility. They have better distribution, more pricing power and have become very effective on social media; all of this matters.

Is China a risk or an opportunity?

We believe China is an incredible opportunity with an element of risk. The propensity of the Chinese consumer to spend in luxury remains very high, the perceived ‘status’ element is just as important as ever, the brands are much better positioned to engage with the ongoing growth (more and improved stores, better digital, more effective on local social media), the price gap versus Europe has shrunk, the household savings rate is very high at over 40% (twice that of Germany), international travel is recovering but at a slower pace, the expansion of the middle class proceeds as expected and there is no evidence that the Communist Party has any concerns (the common prosperity narrative was never anti-luxury but rather anti-the excessive display of wealth and opulence: not the same thing at all). We think China will increase its spend in luxury by almost EUR 80 billion between 2025 and 2029. The risk here would come from a change of policy but we see no evidence that this is the case. A deceleration in spend versus the abnormal peaks is not a risk; we already factor it in.

A sector or stock-led recovery?

As outlined, we think 2024 will see growth below the average but the better brands will continue to outperform. Indeed, we think that while momentum will stay positive in all geographies bar the US (2024 is also a notoriously volatile election year) it is becoming increasingly important to distinguish between the names that have simply benefitted from the general uplift in recent years (ie ‘carried’ by the current as opposed to self-propelled) and those that generally are well-positioned to grow market share further and deliver superior returns even, or rather especially, during more volatile times. Stock picking in 2024 will be more important than at any time since 2016.

Are shares attractively valued?

The recent derating across the board appears to have largely absorbed the expected slower rate of growth, as outlined above, having broadly returned to 2019 valuation levels. We think there is room for further adjustments, but it is particularly the weaker names that are more at risk here. Quality is, and always will be, more defensive and resilient, and yet leave these names in excellent stead for the gradual acceleration we expect to see in H2 2024. The sector remains a solid hedge versus inflation, supported by good cash generation, stronger balance sheets and the capability to support high margins driven by brand clout and underlying demand. Short-term wobbles are exactly that, which is why we are reassured by its time tested track record and very reliable foundations. The luxury consumer ‘’is last in, first out of volatile moments which we are in right now’’ said the CEO of Saks in early November…in other words the last to restrain spending and the first to return…the best type of consumer.

How do we engage to succeed?

The broader definition of luxury brands encompasses both the actual set of brands themselves but also relevant names in adjacent sectors which overlap due to strong appetite from consumers with a very similar profile (ie affluent). We will focus on the more resilient quality names that we think are in a better position to weather current volatility and seek relevant related stories across categories that offer opportunity to secure greater upside.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.