Benign markets are increasingly at odds with the underlying economic picture. GAM Investments’ Julian Howard examines what, if anything, investors should be doing as a result.

23 May 2023

One of supergroup Genesis’s less-known hits of the 1980s was called ‘Land of Confusion’ which described a world in which people are told nothing is wrong despite evidence to the contrary all around them. For investors today, there is a similar dissonance to contend with. Benign stock markets since October, along with low corporate borrowing costs appear to be disguising a host of ills. According to the Bloomberg consensus economic survey, the US economy is now set to grow by just 0.8% in 2024 as the negative effects of recent monetary policy tightening slowly but surely make themselves felt. The US brings further specific risks to the table in the form of an unresolved banking crisis and a hard debt ceiling deadline in early June with no sign of meaningful resolution. Financial commentators frequently talk of inflection points but it is probably true to say that the next few months will determine whether the poor equity market returns of 2022 can finally be vanquished or whether in fact 2023 will be the third year in a row of unexpected economic and market turmoil for this bewildered generation of investors. It seems reasonable therefore to ask whether markets are right to be so relaxed and what, if anything, investors should be doing as a result.

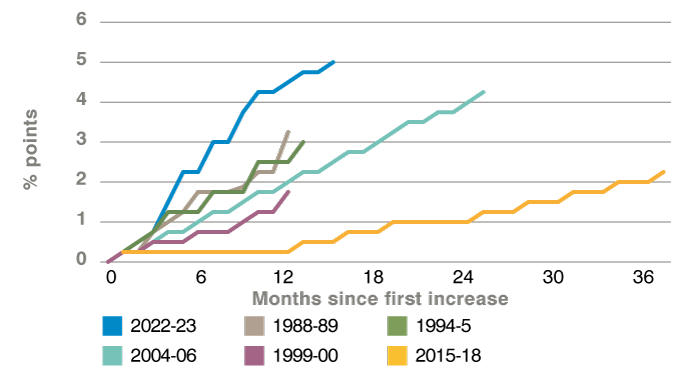

It is of course always easy to be a pessimist and pessimists tend to appear more considered and thoughtful than reckless-sounding optimists. But the reasons to be concerned about the market backdrop today are numerous and bear consideration. Rising interest rates in the US, UK and eurozone are a key concern that cannot just be brushed off. The US Federal Reserve may have recently hinted at a pause in its tightening cycle now that the deposit rate stands at a relatively high 5.25% and headline inflation is hovering just below 5%, but the Bank of England and European Central Bank (ECB) are very much still ‘live’ in their use of monetary policy to tackle price rises. High interest rates are of course a blunt tool, sucking capital out of productive use in favour of sitting on bank deposits or money market funds. This in turn has the potential to slow economic growth, a consequence made all the more likely by turmoil in the US regional banks that is itself the result of said higher rates. The regional banks’ importance stems from their role in lending into the real economy. The banking system’s ‘confidence trick’ relies on depositors keeping their money at an institution. But Silicon Valley Bank’s demise in a matter of days in March could be traced in part to social media encouraging an exodus of depositors in favour of higher rate-paying institutions or money market funds. Unviable banks do not lend money and the sheer pace of interest rate rises in a short period of time is generating prolonged systemic and economic risks from this sector.

Figure 1: Fast and sharp – the nature of this hiking cycle has been without recent precedent

Source: Bloomberg, GAM. Past performance is not an indicator of future performance and current or future trends.

Another casualty of higher rates has been the relative reward investors receive for holding stocks. In the US, the largest region in the MSCI AC World global equity index, the forward earnings yield of the S&P 500 is less than 2% more than the risk-free US Treasury yield of 3.5%. Historically, this has boded ill for future returns in the market, an intuitive point given that investors are unlikely to own more stocks if they can already earn good risk-free rates. The other lurking threat is the US debt ceiling issue. Investors may have become complacent given that previous debt ceiling limits have always been averted at a minute past midnight but the unwillingness of today’s US lawmakers to strike a deal is worrying. This is partly the result of the market not applying the usual pressure. Stock market volatility is low, US Treasury yields have fallen to 3.5% this year and the US dollar, as measured by the Bloomberg dollar index, remains relatively firm on a five-year view. This is giving the impression to those involved in the political process that the markets are ‘okay’ about the situation and increases the possibility that a deal falls through for purely partisan reasons. With a very narrow majority in the House, Republicans may not be in the mood to compromise and could be happy to wreck the current administration’s ambitious spending programme. But the true consequences of a no-deal would be far graver. The Council of Economic Advisors estimates that a protracted US default will cost the US more than 6% points of economic growth.

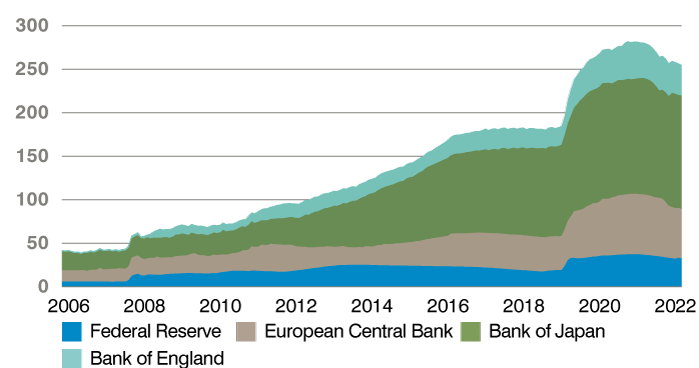

So do equity investors know something the rest of us don’t? It is true that some economic fundamentals remain encouraging. In the US, unemployment stands at just 3.5%, with headline inflation well off last year’s 9% peak at 4.9% today. But these, along with China’s gradual re-opening, somehow feel insufficient explanation for the now-stellar 16.3% return of the MSCI AC World index from 14 October 2022 through to 8 May this year. Similarly, US investment grade and junk firms as of 9 May need only pay 1.6% and 4.7%, respectively, over and above the 10-year US Treasury yield for debt financing, such is lenders’ risk appetite. One plausible explanation for the lack of alarm may be that investors know that long term interest rates, though higher than they were, remain effectively capped and therefore fundamentally supportive of risk assets. This is down to key central banks’ enormous accumulation of bonds after successive bouts of quantitative easing (QE), which has the effect of pushing down yields.

Figure 2: Still holding onto those bonds – bank balance sheets have barely begun to unwind

Source: Bloomberg, GAM. Past performance is not an indicator of future performance and current or future trends.

But even with market interest rates supposedly ‘capped’ by bloated central bank balance sheets, equity earnings yields are just not sufficiently enticing and only deepen the mystery of the benign market backdrop. Another reason might be new artificial intelligence in the form of ChatGPT and others which has, according to a recent National Bureau of Economic Research study, boosted returns for firms with higher exposure to it by 0.4% a day. But markets tend to get over-excited about new innovations in the short term and, if predictions about job disruption become anything like reality, regulation will follow. Perhaps the real lesson here is that sometimes economic and market signals just do not make sense. The pragmatic counter to periods of nonsensical markets is through careful, suitability-driven portfolio construction. Just as for moments of volatility, times of unsettling calm are best handled by focusing less on fevered analysis and trading and more on robust portfolio construction that can handle such periods without deviating from given long term objectives. For most investors this means combining the long run growth opportunity of equities with capital preservation strategies that can smooth out volatility and uncertainty.

For investors who have done this preparatory work in good time, there are two further consolations that the current times can offer. First, contradictory market indicators are arguably a better phenomenon than the overwhelming consensus and complacency that characterised both the late 1990s technology boom and the 2008 Global Financial Crisis. Second, the high interest rates described, while a potential short-term challenge for stock markets (at least in theory), represent a low-risk way of generating consistent returns in the non-equity portion of a blended portfolio, via short-dated fixed income and cash holdings. Today’s land of confusion may prove less memorable than its 1986 musical namesake, but it need not be a source of anxiety for investors either.

Important disclosures and information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers.