GAM Investments’ Julian Howard outlines his latest multi asset views, exploring how central banks’ clumsy attempts to deal with supply-driven inflation are battering growth and could set the world back on the path of secular stagnation

21 July 2022

Review

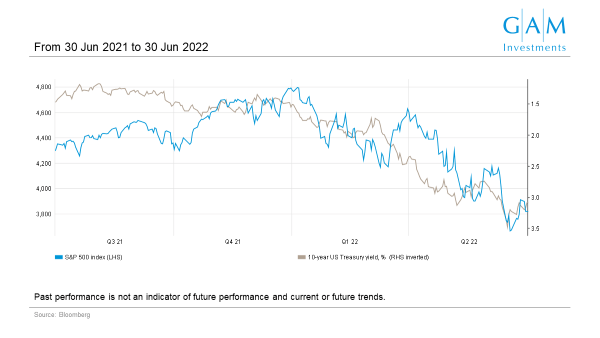

Global equities as measured by the MSCI AC World Index in local currency terms fell -13.5% during the second quarter of the year while bond yields as measured by the 10-year US Treasury note rose from just below 2.4% to just under 3.0% over the same period. As concerns over more enduring inflation mounted, markets rapidly moved to price in expectations of higher interest rates both in the short-term and long-term. Key developed market central banks either tightened monetary policy or signalled that they intended to do so soon, with the Federal Reserve (Fed) raising the discount rate by 75 bps in one move alone in June. That both equities and bonds lost ground was hardly surprising. Both assets are at their core financial instruments with claims on future cashflows, and with prevailing interest rates rising amid uncertainty over where they will peak, current prices naturally had to adjust downwards. At the core of the uncertainty lies the future path of inflation. Notoriously difficult to predict at the best of times, inflation’s trajectory seems even less predictable amid the displaced supply chains and labour markets resulting from the war in Ukraine, strict lockdowns in China and the broader post-pandemic recovery. However, the final weeks of the quarter hinted at what the possible endgame might look like. As US consumer sentiment and spending patterns faltered amid high prices and the running down of pandemic-era savings, surveys and implied market measures of future inflation expectations started to show signs of cooling. In a familiar pattern of bad news equates to good news, equity markets regained some poise on the expectation that inflation may peak soon and both central banks and market-based interest rates would consequently adjust downwards. This shift in market price action was helped further by tentative evidence that the Chinese authorities would seek a more optimal trade-off between virus containment and economic growth. In the US, the Nasdaq Index of technology stocks performed well during this short phase, revealing just how dominant a theme inflation and rate expectations had become during the quarter.

Chart 1: Rising long term rates continued to hurt stocks this quarter

Source: Bloomberg. Data from 30 Jun 2021 to 30 Jun 2022. For illustrative purposes only. Indices cannot be purchased directly.

Views1

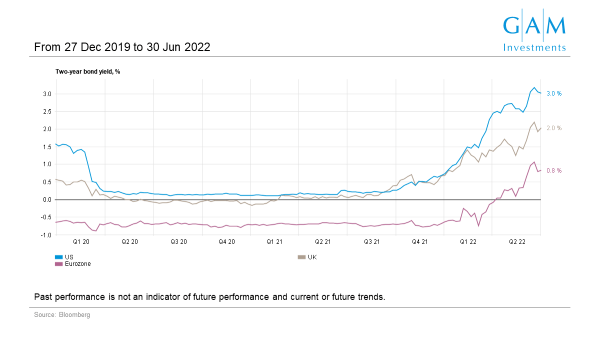

We broadly favoured equities during the quarter; a rotation of some European and emerging market exposure back to US core equities made sense as the risks of a global economic slowdown mounted. However, we continued to focus on the structural growth which can come from US technology and China A stocks as crucially they may potentially have the capacity to thrive in a lower growth environment. Away from equities, in fixed income and credit, we like insurance-linked bonds, mortgage-backed securities, ultra short-dated investment grade paper and, to a lesser extent, government bonds. We favoured very short-dated government bills or money market assets as appropriate over mortgage-backed securities as we believe steering slightly away from exposure to the US consumer and more to rising discount rates which, if 2-year government bond yields are any guide, are set to potentially offer more interesting nominal yields with almost no volatility, could be beneficial. Any increase in cash or cash-equivalent exposure also allows investors to potentially make a rapid re-allocation to equities in the event that valuation models indicate an opportunity amid the prevailing market volatility. In alternative investments, our focus remains on merger arbitrage and convertible arbitrage. While both have, as expected, fared better than main market equities and bonds this year, merger arbitrage has raised some concerns around potential sensitivity to a slowing growth environment.

Chart 2: Two-year government bond yields suggest cash is becoming more interesting

Source: Bloomberg. Data from 27 Jun 2019 to 30 Jun 2022. For illustrative purposes only.

Outlook

As described earlier, the future path of inflation is notoriously difficult to predict and yet it has become the dominating force of the investment landscape and is likely to continue to be so for at least the next few months. Persistently high inflation will likely cause continued consternation as capital markets attempt to price both it and the response to it in, reducing net present values across equities and bonds. Central bank policy could add further fuel to the fire as the US, UK and eurozone economies teeter perilously towards recession. But ironically said recession – or at least curtailed growth – will only accelerate a restoration of pre-2022 conditions. The low growth, low rates and low inflation that have characterised much of the last two decades will probably characterise at least the next two as the world economy grapples with the looming structural challenges of inequality, shrinking workforces and climate change. The current inter-regnum period of post-pandemic, conflict-driven supply disruption will not last forever. Already the last week or so of the quarter under review hinted at this next phase as recession and low growth concerns started to supersede inflation ones. The next few months will see both scenarios continue to fight for market attention before – in our view – the familiar pain of stagnation ultimate prevails. It is then that assets offering secular earnings growth in a low growth world could well resume their ascendancy in investment portfolios.

1 No risk management technique can guarantee the elimination or mitigation of risk in any market environment.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. There is no guarantee that forecasts will be achieved. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Assets and allocations are subject to change. Past performance is no indicator for the current or future development.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. There is no guarantee that forecasts will be achieved. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Assets and allocations are subject to change. Past performance is no indicator for the current or future development.