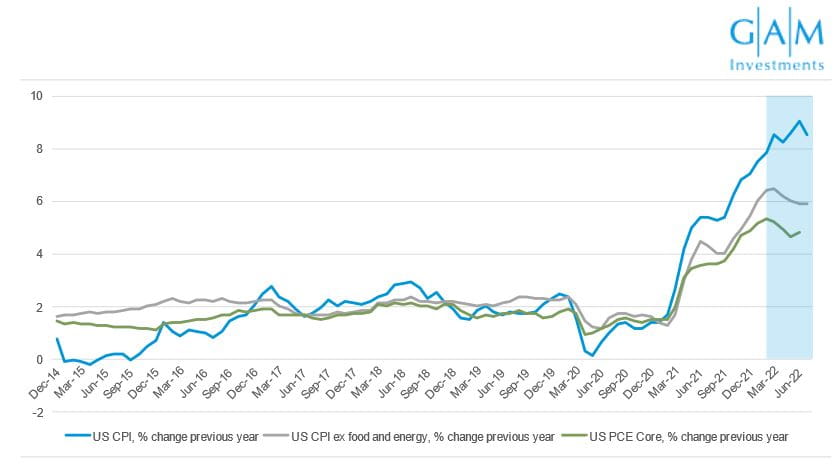

Earlier this month, we saw US CPI soften from a giddy 9.1% rise on the previous year to a slightly more palatable 8.5%. GAM Investments’ Julian Howard considers whether this marks the beginning of the end of the post-pandemic inflation spike, or just a blip in a much longer inflationary era, as well as the implications for investment portfolios.

19 August 2022

In 1980 the economist Julian Simon bet Stanford biologist Paul Ehrlich that five metals (of Ehrlich’s choosing) would fall rather than rise in price over the next decade. At stake was both men’s judgement on the world’s ability to provide sufficient resources for humankind. Ehrlich believed that humanity was a timebomb of resource depletion that would result in inflation and then famine. Simon believed that more humans meant more innovation and therefore new ways to sustain larger populations. Both agreed that the price of the metals would be a fair proxy for who was right. Ultimately, Simon won given the downward trajectory of the five metals in the decade to 1990.

Fast forward to 2022 and the arguments around inflation may be less Malthusian in their tone, but are no less fevered for it. After months of accelerating inflation, there may finally be reasons for optimism. US CPI has at last softened from a giddy 9.1% rise on the previous year to a slightly more palatable 8.5%. Stopping short of double digits is doubtless providing US policymakers with palpable relief, not least the current administration. President Joe Biden had described high inflation as “sapping the strength of a lot of families” and introduced the recently-passed Inflation Reduction Act to deal with the issue. The real (no pun intended) questions now are whether this is the beginning of the end of the post-pandemic inflation spike or just a blip in a much longer inflationary era. And, more importantly, what are the subsequent actionable insights for investment portfolios?

Chart 1. Inflation eases - start of the end, or end of the start?

Source: Bloomberg

As Mr. Ehrlich discovered, regardless of one’s academic credentials, inflation is notoriously hard to predict. With that said, the case for the recent easing continuing into the autumn is compelling. As far as precedents go, today’s inflation doomsayers like to point to the stagflation of the 1970s but there is little evidence of an extended, structural period of inflation taking hold. With expectations a decent prognostic guide to future inflation, the bond markets in the form of the 10-year US Treasury note are implying an average inflation rate over the next decade of just 2.4% as of mid-August. A brief survey of recent drivers of inflation suggests that Clinton political advisor James Carville’s instincts about the bond markets reigning supreme remain correct even today. Higher food and energy costs stemming from the war in Ukraine are showing signs of settling back down even as the conflict persists. According to Bloomberg, wheat futures are down -44% from their early March peak to mid-August as grain shipments from Black Sea ports belatedly resume. Oil futures have also softened, from more than USD 120 a barrel in early June to less than USD 90 in mid-August amid (frustratingly, it must be said) gradual increases in supply from OPEC and US shale producers. Gas is the more stubborn part of the inflation picture given its use by Russia as a means of applying political leverage, particularly against continental Europe. But here too, there could be grounds for optimism with Spain offering to build a new pipeline connecting the Iberian peninsula to France within a nine-month timeframe in an effort to promote more European energy independence.

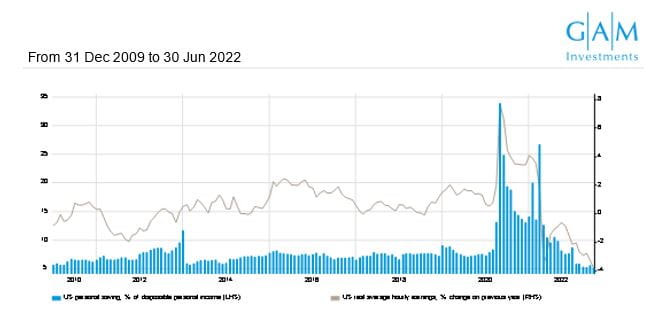

The other major potential driver of disinflation is softer global demand, which itself is the result of monetary policy made tighter in response to yes, inflation. No financial commentary today is replete without mention of impending recession and if inflation is accepted as too much demand versus too little supply then the prospects for inflation cooling soon look promising given the deteriorating demand picture. As US consumers face higher prices, falling real wages and higher debt costs, their pandemic savings are being rapidly eroded. A July 2022 report by Bloomberg Intelligence revealed that Americans were buying less shampoo, laundry detergent and baby nappies, a sure sign of slowing consumption that will eventually take pressure off the price of goods and services. Recession, or at least low economic growth, therefore seems likely in the face of the double onslaught of higher prices and commensurately higher borrowing costs enacted to deal with them. The Federal Reserve has taken to raising discount rates in cool 75 bps increments, as seen in June and July, and adverse personal outcomes are sadly starting to be felt in the form of some consumers’ inability to afford to maintain personal hygiene, as described above. Unpalatable as it may be, the sooner economic growth stalls, the sooner inflation will likely normalise towards levels last seen in 2019. In this sense, the historical precedent for today’s potentially brief-but-ugly spell of inflation is more likely the immediate post-WW2 period when reconstruction aid from the US flooded into shattered Asia and Europe and prices spiked but settled back down again soon after.

Chart 2. Savings rates collapse as US consumers struggle in the face of price increases

Source: Bloomberg

Past performance is not an indicator of future performance or future trends

For investment portfolios, the potential implications are clear. Now is surely not the time to be chasing inflation hedges that in some cases have become relatively expensive. These include, inter alia: FTSE 100 miners and energy firms, certain real estate investment trusts, European utility stocks and government-issued inflation-linked bonds. While these examples have fared well in the first half of 2022 as inflation fears took hold, timing their perfect entry and exit is next to impossible. And structural allocations to these assets would have incurred an opportunity cost amid market conditions characterised by low rates and low inflation, which may yet resume.

Instead, assuming today’s inflation will indeed prove fleeting, a more sensible long term investment approach in our view would be to seek out sources of growth able to thrive in a low growth backdrop. In equities, this would likely include allocations to consistent revenue-generating technology stocks, emerging markets and China. While the latter appear to be themselves a source of low growth in the face of inflexible Covid-zero policies, we believe their long term secular growth case remains undimmed as millions are lifted from poverty and become consumers. Those who remain hesitant to call either accelerating or receding inflation in the face of all the above evidence can still console themselves that equity markets have consistently generated strong real returns over time (source: The Rate of Return on Everything, NBER, 2015) through both inflationary and deflationary periods. This last point may be of little comfort to northern hemisphere consumers facing tough spending choices this winter, but the signs are that the pain may not persist for too much longer. If inflation does continue to soften, central banks will be free of the torture of deciding between controlling prices and maintaining economic growth, and markets will breathe a similar sigh of relief. With luck, investors will not need to place bets on what happens in the next decade.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.