Mortgage-Backed Securities – The senior bonds we focus on are backed by robust mortgages that have substantial home equity and low default risk

December 2023

Challenges and opportunities: Click here to read GAM's investment managers' Outlooks for 2024

The US housing market has been mixed; house prices are rising, but the increase in mortgage rates has posed a challenge to the housing market. Affordability of single-family housing has deteriorated substantially for first time buyers. We saw prices of single-family homes drop modestly, but then quickly followed by seven months of increases this year, largely due to the supply shortage of housing available for sale and rent, plus the pent-up demand for housing among millennials, who are forming new households.

Vacancy rates are at historical lows, and with the strong growth in household formation, a sustained increase in new housing construction is needed. The current increases in construction of single-family housing is not adequate to meet the strong demand. For this reason, we expect a strong support for house prices even if we experience a substantial economic downturn. Our base case for 2024 is a moderate drop in mortgage rates and a stabilisation of prices, as the housing market remains constrained by tight inventory.

We are in favour of securities that are senior in the capital structure and collateralised by seasoned mortgages issued prior to the Global Financial Crisis (GFC) of 2007-2008, while homeowners have a substantial amount of equity in their homes. This provides a strong incentive for homeowners to continue making mortgage payments even in periods of financial stress, to avoid foreclosure. These securities provide significantly more protection against defaults than more recent mortgages in the event of house price declines or recession.

We believe the outlook for these securities is positive for several reasons:

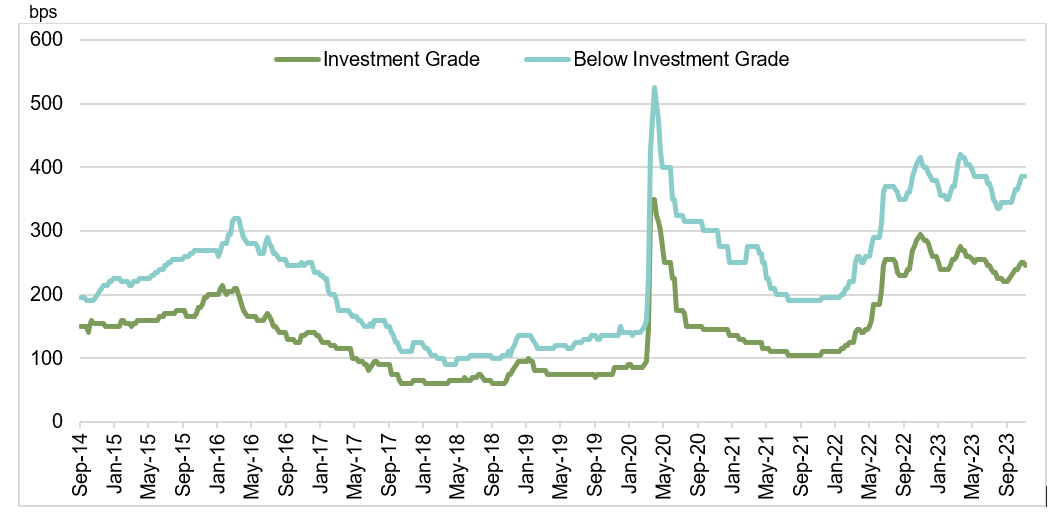

- Legacy Residential Mortgage-Backed Securities (RMBS) spreads are near the wider end of the historical range

- Strong underlying mortgage loans in Legacy RMBS

- Defensive positioning even in a recession

The current wide spreads enable the possibility of capital gains on top of the carry. In addition to the strong underlying credit, we believe that one of the major catalysts for spread tightening will be the dwindling supply of new issue RMBS in the current high interest rate environment.

Legacy RMBS Spreads

Non-Agency

Source: TRACE, Wells Fargo Securities, November 10, 2023. For illustrative purposes only.

Past and current trends should not be relied upon as an indicator of future trends.

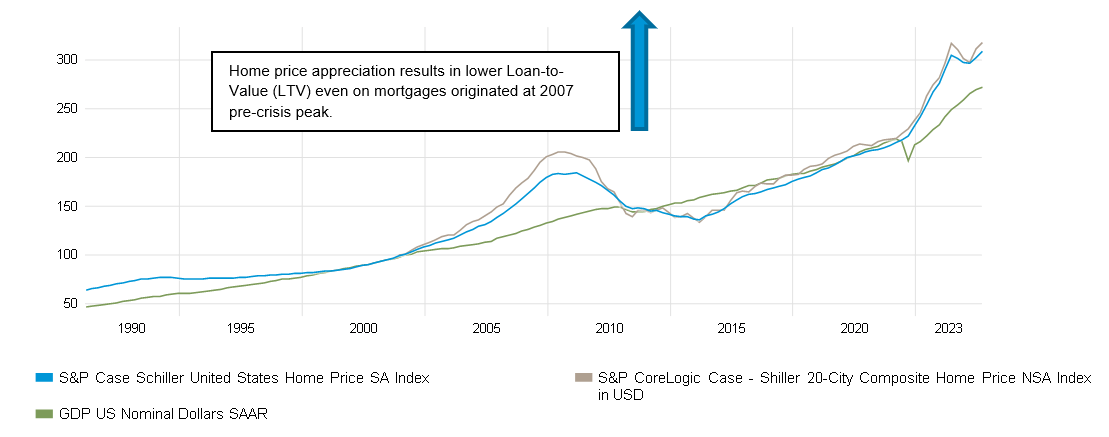

Mortgages originated before 2009 have experienced strong home price appreciation (HPA) over the past 15+ years. On average, a mortgage loan originated at the pre-crisis peak in 2007 will have experienced over 50% HPA. The increase in the underlying home asset value improves the performance of the mortgages through lower delinquency levels and higher recovery levels in the case of a default.

S&P Case Schiller United States Home Price SA Index

Source: Bloomberg.

Past and current trends should not be relied upon as an indicator of future trends.

Past and current trends should not be relied upon as an indicator of future trends.

The senior bonds we focus on are backed by robust mortgages that have substantial home equity and low default risk, as discussed above. The current economic conditions of low unemployment, low household debt and high savings also support the creditworthiness of the securities, even in the event of a recession. Moreover, the average mortgage we invest in has a sufficient value cushion to withstand a potential decline in home prices that exceeds the magnitude of the GFC.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

Indices referenced herein are provided for illustrative purposes only, are unmanaged and do not incur management fees, transaction costs or other expenses associated with a portfolio. Therefore, comparisons to indices have limitations.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio nor represent any recommendations by the portfolio managers nor a guarantee that objectives will be realized.

Indices referenced herein are provided for illustrative purposes only, are unmanaged and do not incur management fees, transaction costs or other expenses associated with a portfolio. Therefore, comparisons to indices have limitations.

This material contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.