Julian Howard, GAM’s Lead Investment Director of Multi-Asset Class Solutions (MACS) London, outlines his latest multi-asset views, exploring how the economy is growing without excess inflation and markets are progressing despite high interest rates.

05 April 2024

Review

Global equities, as measured by the MSCI All Country (AC) World Index, posted a robust +9.6% gain in local currency terms in the first quarter of 2024. The single strongest regional gain came from Japan, which benefited from improving global growth, improved corporate governance and a (finally) normalising inflation and rates environment. Europe also picked up but it was the US that made the strongest contribution to market progress given its two thirds allocation within the MSCI AC World Index. The S&P 500 was up +10.6% over the review period, with the Nasdaq 100 technology Index up +8.7%. Justifying continued gains in a rally now dating back to October 2022 is on the surface challenging, with US interest rates standing at an elevated 5.25% and valuations becoming increasingly stretched. By the end of the review period, the forward earnings yield on the S&P 500 was 4.6%, offering investors just 0.4% more yield than the 10-year US Treasury’s risk-free 4.2%. Similarly, the Shiller CAPE, or cyclically-adjusted price earnings ratio, stood at 34, above the 30-year average of 28. How did stocks get to this point without a serious adjustment? We would note that a potentially significant change may have altered the usual dynamics in both the economy and markets in recent months, in the form of increased productivity.

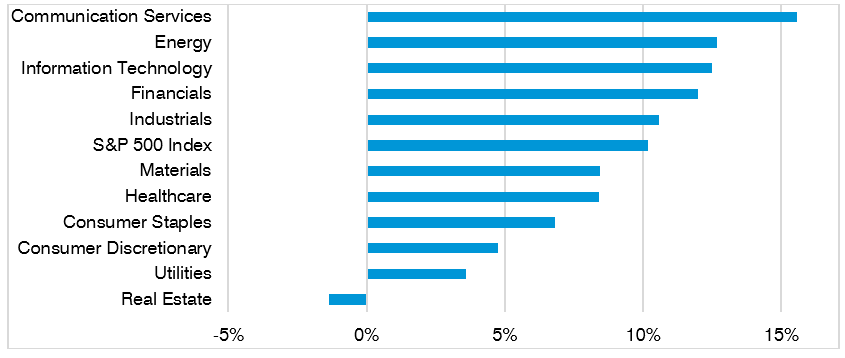

In the US, output per hour worked has been steadily rising and, combined with strong consumption, appears to have created a ‘Goldilocks’ environment of improving economic growth without changing the generally stabilising course of inflation. Much of the improved productivity can be put down to post-pandemic supply chain normalisation but the case for a growing contribution from the gradual adoption of artificial intelligence (AI) across the economy is also strong. A poll by the US Census Bureau in late February reported that nearly 5% of firms had made use of AI in the previous two weeks to produce goods and services. Markets both drove and reflected these developments. Most obviously, ‘picks and shovels’ providers of AI technology and infrastructure have led US stocks to both strong earnings and the prospect of more in the near future. Nvidia is a case in point, but it should also be noted that participation in the S&P 500’s gains is starting to extend beyond just technology. Sectors such as industrials, energy and materials have all posted gains in excess of +8% this year to end March, suggesting that cyclical parts of the stock market which more closely reflect the state of the real economy somehow did not feel the usual need to worry about inflation or interest rates anymore. The rally in other words began to show signs of a more profound sustainability.

Chart 1: Not just technology enjoying the productivity party this year

S&P 500 sector price return from 29 December 2023 to 31 March 2024

Source: Bloomberg.

Not another dot-com bubble (at least not yet)

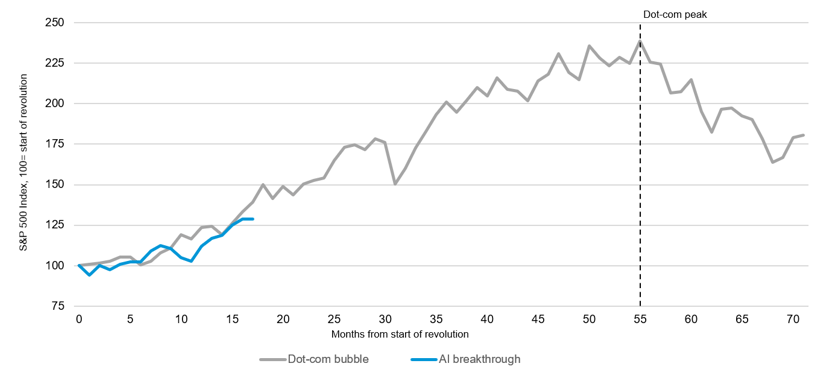

The US, and US technology in particular, has of course been a significant contributor during the review period. Philosophically it is worth noting that we have not ‘played AI’ per se, but instead captured the trend by virtue of our deliberate exposure to the unique powerhouse of US innovation generally, whatever the specifics are from one year to the next. As it happens, we do not equate today’s run-up in technology stocks with the dot-com bubble of the late 1990s but somewhat extended valuations and the duration of the rally (since October 2022) make it particularly important from a risk management perspective that the capital preservation sleeve of our portfolios performs consistently and reliably.

Chart 2: S&P 500 from 31 January 1996 to 31 March 2024

Source: Bloomberg. ‘Start of revolution’ = Telecommunications Act end Jan 1996 for dot-com bubble and introduction of ChatGPT end November 2022 for AI breakthrough.

Outlook

As cliched as it may sound, markets probably are now at a pivotal moment. Price appreciation can only go on so long without some confirming evidence coming due. While the inflation and rates debate has been raging since the end of the pandemic, the more proximate determinant of what happens next could well be the future course of productivity. If the rebound in productivity observed in the last couple of years peters out as the tailwind of supply chain normalisation fades, and AI adoption stalls amid a realisation that it was not so transformative after all, then markets will surely turn their full attention back to that 5.25% Fed Funds rate and the Federal Reserve’s apparent reluctance to quickly unwind all of it in short order. If however, the gains in productivity can be continued into the rest of the year thanks to the widespread take-up of AI into even more aspects of economic activity, then the rally could propel itself anew. Economists have concerned themselves with the so-called ‘productivity puzzle’ on both sides of the Atlantic since the aftermath of the global financial crisis (GFC), primarily because its absence seemed to be holding back a true restoration of pre-GFC trend economic growth. Should the productivity puzzle actually be solved this year, it will potentially create a set of near-perfect economic and market conditions, for the US at least. High productivity would afford the US economy the means of growing without generating undue inflation and the adverse consequence of higher interest rates. Stocks will benefit not just because listed technology corporations will continue to supply and improve the AI ‘product’ but also because other cyclically-sensitive sectors will also be able to grow without butting up against higher inflation and rates. As this plays out, investors will still need to contend with an unedifying conveyor belt of geopolitical risks.

The Middle East remains volatile, US-China relations are poor and unlikely to improve post-November and then of course there is November itself. A Trump win would bring tax cuts on the one hand, but higher fiscal deficits, tariffs and general policy ambiguity on the other. One consolation of all this is that America’s exceptionalism seems to allow recklessness and uncertainty to go unpunished. This is nowhere better exemplified than in its markets which we are confident will remain focused on cold, hard fundamentals. The US therefore offers an ironic haven from what could be a bumpy few months ahead in the geopolitical sphere. And beyond the noise, the prospect of a genuinely new economic era could be quietly unfolding.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The MSCI AC World Index is a stock index that captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. With 2,921 constituents, the index covers approximately 85% of the global investable equity opportunity set. The S&P 500 Index is a stock index tracking 500 of the largest, publicly traded companies in the United States.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The MSCI AC World Index is a stock index that captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. With 2,921 constituents, the index covers approximately 85% of the global investable equity opportunity set. The S&P 500 Index is a stock index tracking 500 of the largest, publicly traded companies in the United States.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

This article contains forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This disclosure shall in no way constitute a waiver or limitation of any rights a person may have under such laws and/or regulations.

In the United Kingdom, this material has been issued and approved by GAM London Ltd, 8 Finsbury Circus, London EC2M 7GB, authorised and regulated by the Financial Conduct Authority.