US stocks have been defying higher interest rates consistently since October 2022, rising by around 40%. At the same time, the US economy has accelerated even as inflation has been cooling. Either something is about to break, or a profound change could propel stocks onwards.

10 April 2024

Consider the following: in the 12 months to 22 March 2024, the MSCI AC World Index has risen a cool +29.2% in local currency terms. In the US, the S&P 500 Index posted a 35.1% gain and the Nasdaq 100 Index of technology-focused stocks +47.2% (source: Bloomberg, GAM). Compare this with the observed rate of annualised returns from stocks over multi-decade periods; around 7% according to respected sources such as the Nation Bureau of Economic Research’s ‘The Rate of Return On Everything 1870-2015’ and Jeremy Siegel’s buy-and-hold bible ‘Stocks for the Long Run’. The history-defying performance of the last year has been delivered more through price than earnings gains: the S&P 500’s forward earnings yield (essentially expected profits relative to the share price) was 4.6% as at 22nd March, just 0.4% more than the 10-year US Treasury bond yield (the so-called ‘risk-free’ rate) of 4.2% (source: Bloomberg, GAM). That thin 0.4% risk premium is all that investors now get for incurring the risk of holding stocks versus the guaranteed return of US Treasuries. Another key valuation gauge, the Shiller CAPE (the cyclically adjusted price earnings ratio for the S&P 500) stands at an elevated 34x as at 1st March, well above the 30-year average valuation of 28x (source: Bloomberg, GAM).

Ever-higher valuations need a gamechanger. AI could be it

The facts alone above logically suggest a future adjustment in the rate of ascent of markets, if not an outright correction. But investors might wish to pause at this point. Is this really a doomed re-run of the late 1990s when valuations seemingly did not matter, until suddenly…they did? Back then firms like Pets.com (in)famously soared but never made meaningful – or indeed any – profits. And everyone knows what happened next. Or are we instead on the cusp of a discrete new economic era worthy of splicing onto late economist Walt Rostow’s seminal ‘Stages of Economic Growth’ thesis? Artificial intelligence (AI) is already changing the world in ways unimaginable just a few years ago, with tentative signs that the years-long search for improved productivity may finally be coming to an end. Whisper it, but could the rally actually continue?

Wars and politics – there is plenty to fret about in the world

In investments, just as in other areas of life, pessimism tends to sound savvy and realistic while optimism in turn can come across as reckless and naive. And pessimism today is in abundant supply. Starting with the geopolitical backdrop, there are plenty of external factors for investors to fret about. The trade war between the US and China rumbles on and is unlikely to fade in the event of a Republican win in November’s election. Donald Trump has openly talked about a blanket 10% tariff on imported goods since early February, declaring his desire to “completely eliminate dependence on China in all critical areas”. This is likely to be inflationary given the probable targeting of strategic goods such as semiconductor devices and other electronics, steel and pharmaceuticals, even if non-strategic goods like textiles and toys are left out. And then real wars are of course in progress across Ukraine and the Middle East, not to mention areas of Africa and most recently Haiti’s collapse into total anarchy, threatening stability in America’s back yard. The post-WW2 liberal free market order seems to be being replaced with nationalism, protectionism and a distinct lack of global consensus on almost anything.

Rising tide is carrying some ships better than others

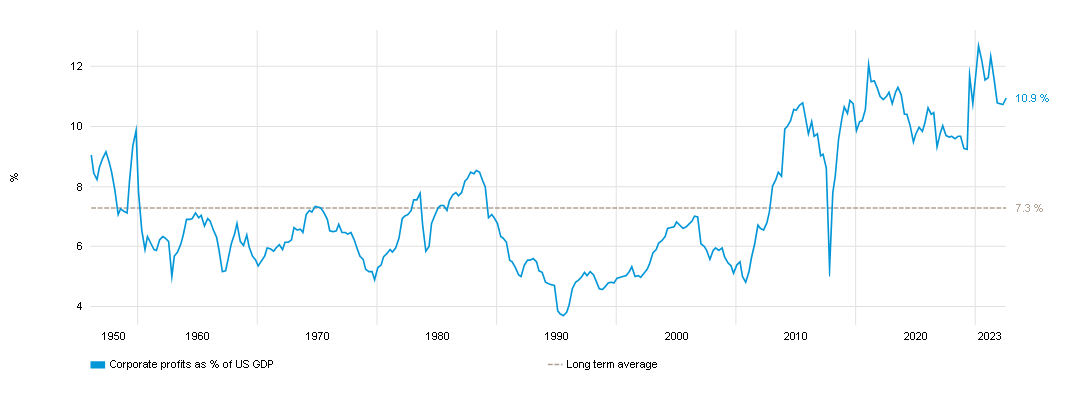

Turning to markets themselves, a long era of very low interest rates has given way to (for now) higher ones with the Fed Funds rate at 5.25% and overnight interest rate swaps markets no longer pricing in imminent cuts amid mixed inflation signals. This is piling theoretical pressure on US stocks in particular which, as outlined above, cannot currently provide an earnings yield that looks attractive compared to risk-free rates. And then there is the concentration problem. Over the last year to 22nd March, the S&P 500’s price appreciation has been driven primarily by three market sectors – technology, communication services and consumer discretionary. This concentration feels like the opposite of the diversification every investor is told should be their goal in constructing a sustainable portfolio. For the market rally to become more sustainable, or indeed continue, corporate earnings need to grow, and preferably diversify too. In the US at least, the latter looks like a big ask given that corporate profits as a percentage of GDP are already elevated, thanks in large part to technology companies. Today, profits stand at 11%, above the long-term average of 7% since 1947 (source: Bloomberg, GAM).

Can profits really go higher from here?

From 1 Jan 1947 to 1 Jul 2023

Source: St. Louis Fed

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

Solving the productivity puzzle at last?

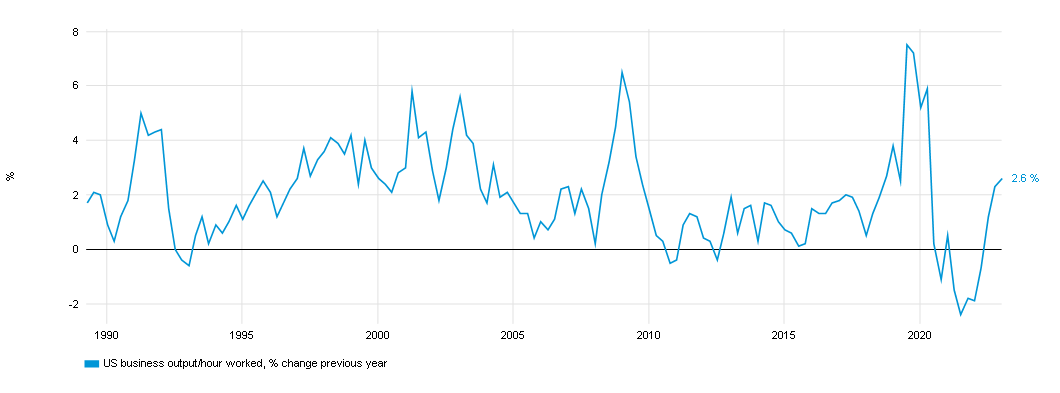

The threshold for stocks to be able to make progress from here is therefore high. But there is an emerging trend that could meet that threshold, and that trend is rising productivity. In the US, output per hour worked has been improving since mid-2022, and this offers a compelling explanation for how the economy has been able to grow at an annualised rate of 3.2% in the final quarter of 2023 without incurring additional inflation. Indeed, headline CPI inflation on the previous year has come down from 9.1% in mid-2022 to 3.2% by February this year (source: Bloomberg, GAM). A sizeable part of the productivity pick-up has undoubtedly come from supply chains normalising post-pandemic, and this can duly be seen in stabilising goods inflation. But some is likely also coming from AI which is gradually infiltrating all sectors in the economy. This raises the tantalising prospect of any further strengthening in US economic growth being unimpeded by inflation. This would be profoundly significant because a strong economy less likely to generate inflation is also one less likely to be burdened by higher interest rates in the future. This is a true ‘goldilocks scenario’ and explains economists’ long obsession with the productivity puzzle, which may possibly now have been solved.

Could AI ‘trickle down’ broaden – and sustain – the rally?

A strong economy unimpeded by the prospect of much higher inflation or rate rises also bodes well for corporate earnings generally, and offers a neat explanation as to how even cyclical sectors like financials, industrials and materials have started to perform better recently, if not quite as well as technology itself. The latter of course has benefited from involvement in the ‘picks and shovels’ aspects of the AI revolution, generating large and stable profit streams that have resulted in them dominating the stock market. Nvidia in particular has been extremely profitable through not even having to compete on price given its dominant market position in supplying AI-suitable chips. This is no re-run of Pets.com. Combined, these productivity and related AI developments go a long way to explaining how the stock market has been able to progress even amid relatively high rates, confounding the pattern of the last few decades in which low rates = good for markets and high rates = bad for markets.

Stabilising supply chains and AI have contributed to a productivity rebound:

From 30 Mar 1990 to 31 Dec 2023

Source: Bureau of Labor Statistics

Past performance is not an indicator of future performance and current or future trends.

Past performance is not an indicator of future performance and current or future trends.

The Dot.com boom casts long shadows and investors should always be wary of breathless talk of ‘new paradigms’ and this time somehow being ‘different’. Valuations today are objectively elevated and stock market concentration is not especially healthy. Politics remains almost hopelessly fractured and November’s US election result is unlikely to change that. But something that marks out the last year or so in both the US economy and stock market is their emerging ability to make progress unaffected by their usual respective nemeses of inflation and interest rates. Some evidence of speculative fever in the stock market exists but that can hardly be applied to a growing economy that is not stoking inflation. Instead, a common factor makes for the more convincing explanation as to why the US economy and markets have both been able to throw off their traditional shackles to further progress and that is where the productivity story comes in. The impact of technologies of course takes time to assess, and large language models are proving not to be problem free. But it is becoming clear that something new may be happening with productivity that transcends mere post-pandemic normalisation. At worst, recent market gains can probably now be justified up to this point, which should make investors less jumpy when asking themselves how they got here. At best, there could yet be more to come.

Important disclosures and information

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

The information contained herein is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained herein may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information contained herein. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice or an invitation to invest in any GAM product or strategy. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. Specific investments described herein do not represent all investment decisions made by the manager. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. No guarantee or representation is made that investment objectives will be achieved. The value of investments may go down as well as up. Investors could lose some or all of their investments.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.